Official Promissory Note Form

Official Promissory Note Form

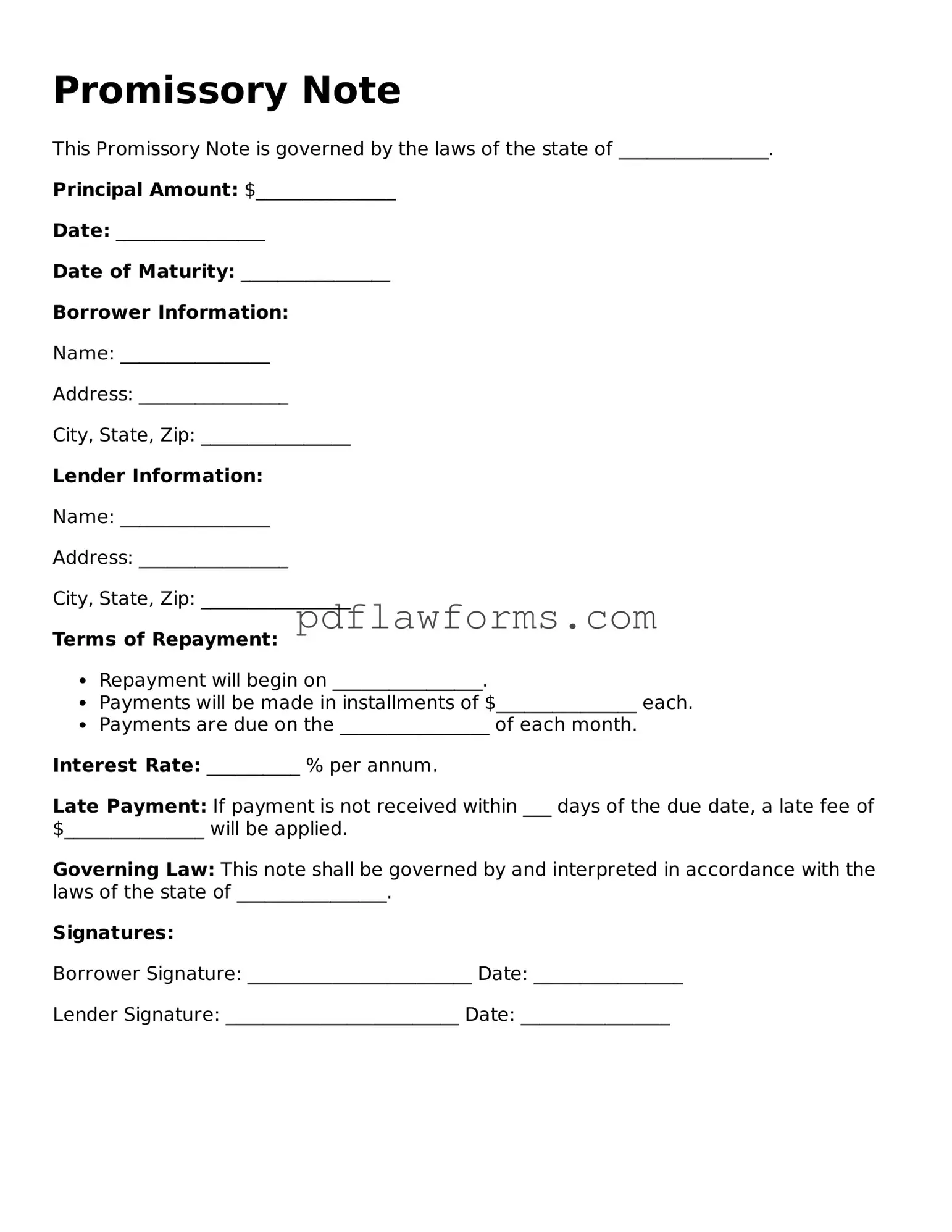

A Promissory Note is a vital financial instrument that outlines the terms of a loan agreement between a borrower and a lender. This document serves as a written promise from the borrower to repay a specified sum of money, typically with interest, by a predetermined date. Key components of a Promissory Note include the principal amount, interest rate, repayment schedule, and the parties involved. Additionally, it may specify the consequences of default, such as late fees or legal actions. Clarity and precision are crucial in drafting this form, as it establishes the legal rights and obligations of both parties. Understanding the nuances of a Promissory Note can help individuals and businesses navigate financial transactions effectively, ensuring that both lenders and borrowers are protected under the agreed-upon terms.

Promissory notes are common financial instruments, but several misconceptions surround their use and purpose. Here are seven prevalent misunderstandings:

Understanding these misconceptions can help individuals navigate the complexities of promissory notes more effectively.

Filling out a Promissory Note can seem straightforward, but many people make common mistakes that can lead to complications down the line. One frequent error is failing to clearly state the loan amount. When the amount is ambiguous or incorrectly written, it can create confusion and disputes later. Always double-check that the number is both written in digits and spelled out in words to avoid any misunderstandings.

Another common mistake is not including a payment schedule. A Promissory Note should specify when payments are due and the frequency of those payments. Without this information, it becomes unclear when the borrower is expected to pay back the loan. This can lead to frustration for both parties. Clearly outline the payment terms to ensure everyone is on the same page.

Many individuals also overlook the importance of including interest rates. If the note does not specify whether the loan is interest-bearing or not, it can lead to disputes over how much the borrower owes. If interest is applicable, it should be clearly stated, including the rate and how it will be calculated. This clarity helps prevent misunderstandings about the total amount due.

Lastly, signatures are often a point of contention. A Promissory Note is not valid without the appropriate signatures from both the borrower and the lender. Some people forget to sign or fail to have a witness or notary present when signing. This oversight can render the document unenforceable. Always ensure that all necessary signatures are present before considering the note complete.

Once you have your Promissory Note form ready, it's important to complete it accurately to ensure all terms are clear. This document will outline the agreement between the lender and the borrower, establishing the repayment terms. Follow these steps to fill out the form correctly.

After completing the form, ensure both parties retain a signed copy for their records. This will help prevent misunderstandings in the future. It's always a good idea to keep communication open regarding the terms outlined in the note.

High School Transcript - Can influence potential career paths based on academic strengths.

To facilitate a smooth transaction, you may want to consider using a complete mobile home ownership transfer checklist that includes the Mobile Home Bill of Sale. This form guarantees that all essential details regarding the sale are captured accurately, ensuring both the buyer and seller are fully informed of their rights and responsibilities.

Affixture - Filing the Affidavit of Affixture is necessary for securing financing on a mobile home affixed to land.

Bill of Sale for a Car - A Bill of Sale can provide peace of mind to both parties involved.