Official Promissory Note for a Car Form

Official Promissory Note for a Car Form

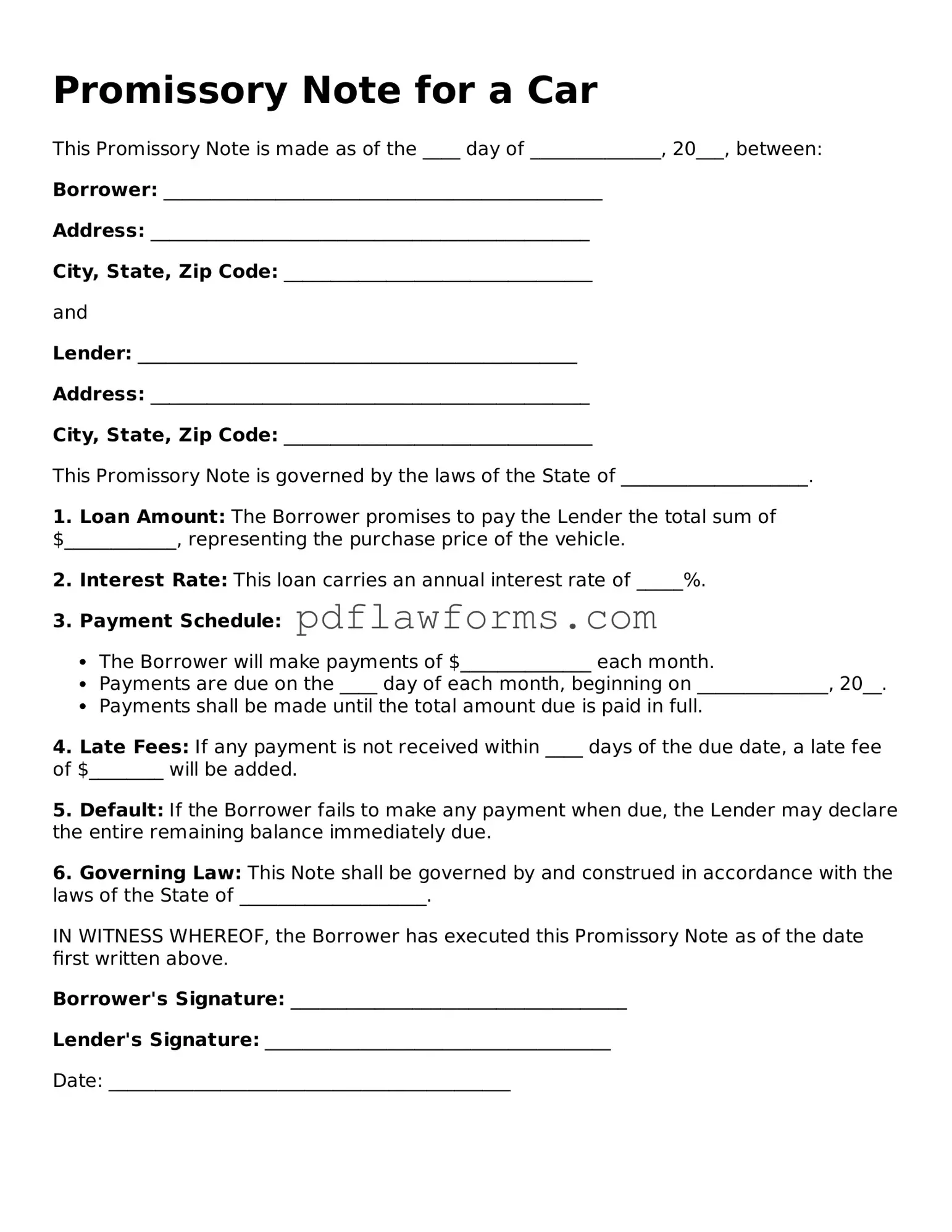

When purchasing a vehicle, a Promissory Note for a Car serves as a crucial document that outlines the terms of the loan agreement between the buyer and the lender. This form details the amount borrowed, the interest rate, and the repayment schedule, ensuring both parties understand their obligations. It includes essential information such as the names of the borrower and lender, the vehicle's description, and any collateral involved. Additionally, the note specifies the consequences of defaulting on the loan, providing a clear framework for both parties in case of missed payments. By formalizing the agreement, this document protects the interests of the lender while giving the borrower a structured plan to follow. Understanding the components of a Promissory Note for a Car can help buyers navigate the financing process with confidence and clarity.

Understanding the Promissory Note for a Car form is essential for both lenders and borrowers. However, several misconceptions can lead to confusion. Below is a list of common misconceptions along with clarifications.

By addressing these misconceptions, individuals can approach the process of securing a car loan with a clearer understanding, ultimately leading to more informed financial decisions.

Filling out a Promissory Note for a Car can seem straightforward, but many people encounter pitfalls that can lead to confusion or even financial issues down the road. One common mistake is failing to include all necessary details. A Promissory Note should clearly outline the terms of the loan, including the amount borrowed, interest rate, payment schedule, and any penalties for late payments. Omitting even one of these critical details can create misunderstandings between the borrower and lender.

Another frequent error occurs when individuals do not read the form carefully. It’s easy to overlook specific clauses or requirements that may not seem immediately relevant. For instance, some notes may include provisions regarding default or collateral. Ignoring these sections can lead to unexpected consequences if a borrower finds themselves unable to meet their obligations.

Inaccurate information is another significant issue. Borrowers often make mistakes when entering their personal information, such as names, addresses, or Social Security numbers. These errors can complicate the loan process and may even result in legal complications. Ensuring that all information is correct and up-to-date is crucial for a smooth transaction.

Lastly, many people forget to sign and date the Promissory Note. This step might seem trivial, but without a signature, the document lacks legal enforceability. Both parties should ensure that they sign the note, acknowledging their agreement to the terms outlined. A missing signature can render the entire document void, leaving both parties in a precarious position.

Filling out the Promissory Note for a Car form is a straightforward process that requires careful attention to detail. Once completed, this document will serve as a formal agreement between the buyer and the seller, outlining the terms of the loan for the vehicle. Follow the steps below to ensure accurate completion of the form.

Release of Promissory Note - The Release of Promissory Note signals the successful conclusion of a financial agreement.

To ensure a smooth loan transaction in Maryland, it is important to utilize a formalized document like the Maryland Promissory Note. This document clearly outlines the obligations of both the borrower and lender, detailing the borrowed amount, interest rate, and repayment terms. For your convenience, you can access additional resources and necessary forms, such as All Maryland Forms, that can assist you in creating a legally binding agreement.