Fill Your Profit And Loss Template

Fill Your Profit And Loss Template

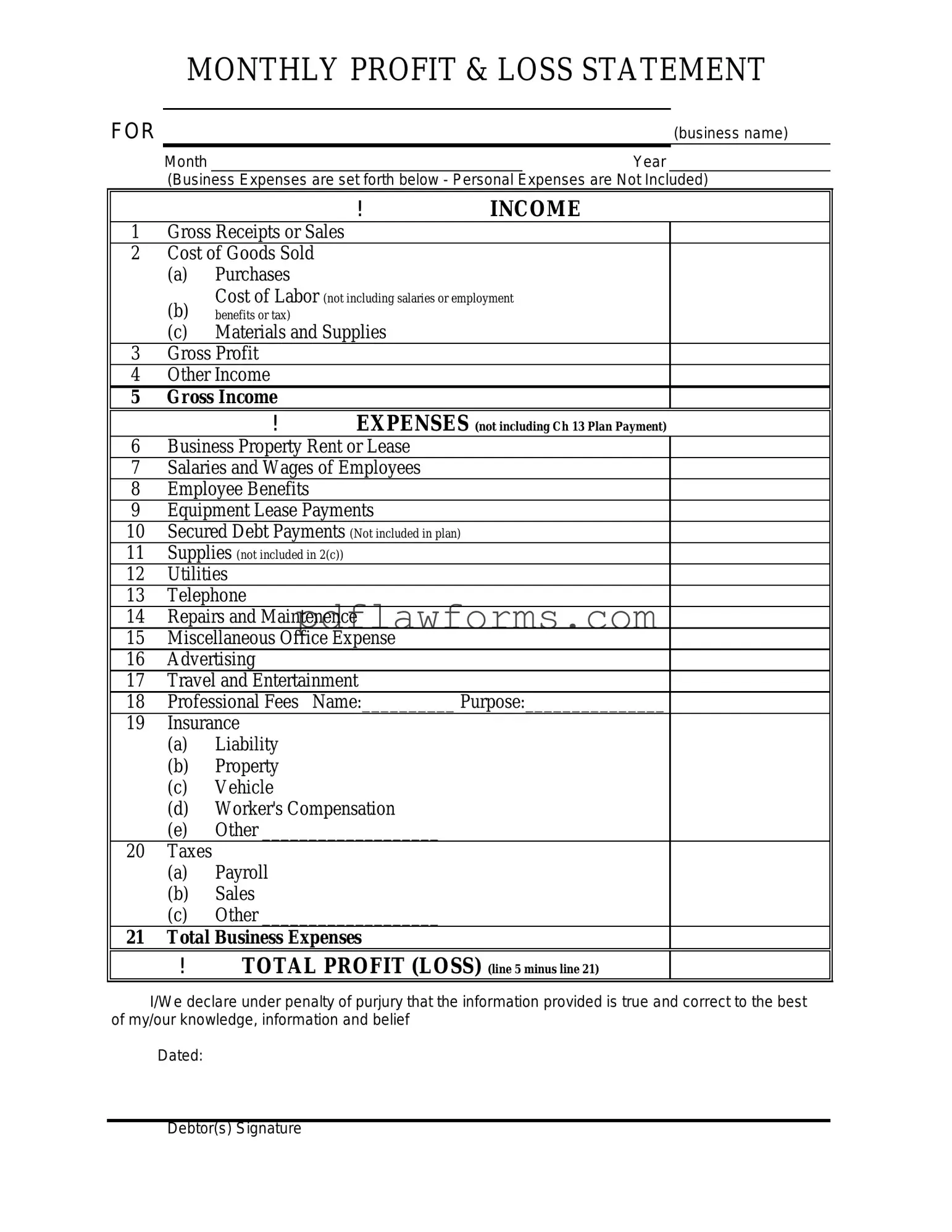

The Profit and Loss form, often referred to as the P&L statement, serves as a crucial financial document for businesses of all sizes. This form provides a clear snapshot of a company's revenues, costs, and expenses over a specific period, typically a month, quarter, or year. By detailing income from sales and subtracting the costs associated with generating that income, the P&L helps to determine whether a business is operating at a profit or a loss. Major components of the form include total revenue, cost of goods sold (COGS), gross profit, operating expenses, and net income. Each section plays a vital role in illustrating the financial health of the business. For instance, understanding gross profit allows owners to assess how efficiently they are producing goods or services. Meanwhile, operating expenses provide insight into the costs necessary to run the business, which can inform strategic decisions moving forward. Overall, the Profit and Loss form is an indispensable tool for business owners, investors, and stakeholders alike, offering a comprehensive overview of financial performance and guiding future planning.

The Profit and Loss (P&L) form is an essential financial document for businesses, yet several misconceptions surround its purpose and function. Understanding these misconceptions can help individuals and business owners better utilize this important tool.

This is not accurate. The P&L form provides a comprehensive overview of both revenue and expenses. It details how much money a business earns and what it spends, ultimately showing whether the business is profitable or not.

Many believe that only large corporations need a P&L statement. In reality, any business, regardless of size, can benefit from maintaining a P&L. Small businesses and freelancers can use it to track their financial health and make informed decisions.

These two documents serve different purposes. The P&L focuses on income and expenses over a specific period, while the balance sheet provides a snapshot of a company's assets, liabilities, and equity at a single point in time.

While the P&L can help in preparing taxes, it is also a valuable tool for internal analysis. Business owners can use it to assess performance, identify trends, and make strategic decisions.

Some people think that P&L statements are only relevant when compiled annually. However, they can be prepared monthly or quarterly, allowing businesses to monitor their financial performance more closely and make timely adjustments.

Filling out a Profit and Loss form can be a straightforward task, but many individuals and businesses make common mistakes that can lead to inaccuracies. One frequent error is failing to categorize income and expenses correctly. When entries are not placed in the right sections, it can skew the overall financial picture. For instance, mixing personal expenses with business expenses can lead to confusion and misrepresentation of the business's financial health.

Another mistake often seen is neglecting to include all sources of income. Some may forget to account for side projects or additional revenue streams. This oversight can result in an incomplete view of profitability. It’s essential to take the time to gather all income sources to ensure that the Profit and Loss statement reflects the true financial status.

People also frequently underestimate expenses. It’s easy to overlook smaller costs, such as subscriptions or minor supplies, thinking they don’t significantly impact the bottom line. However, these small expenses can add up over time, and failing to include them can lead to an inflated perception of profitability.

Additionally, many individuals forget to update their forms regularly. A Profit and Loss statement is most useful when it reflects current data. Relying on outdated information can lead to poor decision-making and financial planning. Keeping the form updated ensures that stakeholders have the most accurate information at their fingertips.

Some individuals may also struggle with the timing of income and expenses. Recording transactions in the wrong period can distort the financial picture. For example, if income earned in one month is recorded in the next, it can create a misleading representation of cash flow and profitability for each period.

Another common error involves not reconciling the Profit and Loss statement with bank statements or other financial records. This step is crucial to ensure that all entries are accurate and accounted for. Discrepancies can arise, and failing to address them can lead to significant issues down the line.

Lastly, many people overlook the importance of reviewing and analyzing the completed form. Simply filling out the Profit and Loss statement is not enough. It’s vital to understand what the numbers mean and how they impact the overall business strategy. Regular analysis can reveal trends and areas for improvement, ultimately leading to better financial decisions.

Completing the Profit and Loss form is an essential step in understanding your financial performance over a specific period. This process involves gathering your financial data and accurately entering it into the designated sections of the form. Following the steps below will help ensure that your submission is thorough and correct.

Employee Time Card Template - Track sick leave and vacation days with ease.

To facilitate a smooth transaction, it is recommended to utilize resources such as the Templates and Guide, which provide helpful insights and templates for completing the California Motorcycle Bill of Sale accurately and efficiently.

Transfer of Shares Form - Establish a straightforward process for recording stockholder information.