Fill Your Mortgage Statement Template

Fill Your Mortgage Statement Template

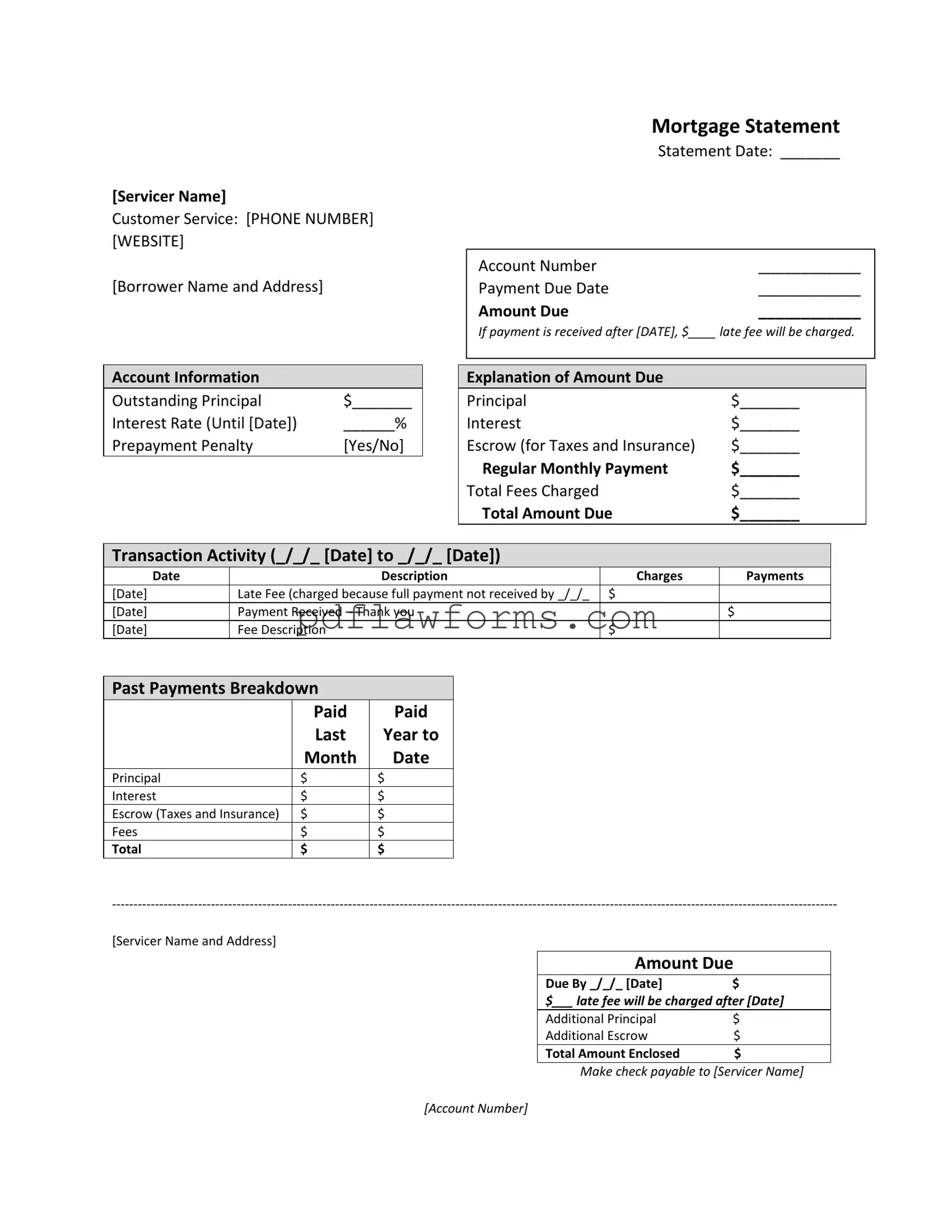

The Mortgage Statement form serves as a vital document for homeowners, providing a comprehensive overview of their mortgage account. At the top, you'll find essential details such as the servicer's name, customer service contact information, and the borrower's name and address. The statement date, account number, and payment due date are prominently displayed, along with the amount due. Homeowners should pay close attention to the late fee policy, which outlines the financial implications of late payments. The form breaks down account information, including outstanding principal, interest rate, and whether a prepayment penalty applies. A detailed explanation of the amount due is provided, listing principal, interest, escrow for taxes and insurance, and total fees charged. Transaction activity is meticulously recorded, showing recent charges and payments, which helps borrowers track their payment history. Additionally, the form includes important messages regarding partial payments and delinquency notices, emphasizing the significance of timely payments. For those facing financial difficulties, resources for mortgage counseling are available, underscoring the servicer's commitment to assisting borrowers in maintaining their homes.

Understanding your mortgage statement is crucial for managing your home loan effectively. However, several misconceptions can lead to confusion. Here are eight common misunderstandings about mortgage statements:

Being aware of these misconceptions can empower homeowners to manage their mortgage more effectively and avoid potential pitfalls.

Completing a Mortgage Statement form can be a daunting task, and mistakes can lead to confusion and potential financial consequences. One common mistake is failing to provide accurate personal information. It is essential to ensure that the borrower name and address are entered correctly, as any discrepancies can delay processing and communication.

Another frequent error involves overlooking the account number. This number is crucial for identifying the loan and ensuring that payments are applied correctly. Omitting or miswriting the account number can lead to misdirected payments and unnecessary fees.

People often neglect to check the payment due date. This date is critical for avoiding late fees. If the form is filled out incorrectly, it may lead to missed payments and additional charges. Always verify the due date listed on the statement to ensure timely payments.

Many individuals also fail to review the amount due section carefully. It is important to confirm that the total amount reflects all charges, including principal, interest, and escrow. Errors in this section can result in underpayment, which may lead to penalties.

Another common mistake is misunderstanding the prepayment penalty section. Borrowers should clarify whether their mortgage includes such a penalty. Failing to understand this could result in unexpected costs if they decide to pay off their loan early.

In the transaction activity section, people often miss reviewing the charges and payments accurately. It is vital to ensure that all transactions are recorded correctly. Discrepancies can lead to confusion about the current balance and payment history.

When it comes to past payments, individuals sometimes overlook the breakdown of payments made over the last year. This information is essential for tracking payment history and ensuring that all amounts have been credited appropriately.

Another mistake involves ignoring the delinquency notice. This section provides important information about the status of the mortgage. If the notice indicates that payments are overdue, immediate action is required to avoid further penalties or foreclosure.

People frequently forget to include the total amount enclosed when sending payments. This can lead to partial payments being applied, which are not credited to the mortgage until the full amount is received. Always double-check that the total matches what is due.

Lastly, many borrowers overlook the information about financial assistance available for those experiencing difficulties. This section can provide valuable resources and support, helping individuals navigate challenging financial situations.

Completing the Mortgage Statement form is essential for managing your mortgage account effectively. Follow these steps to ensure all necessary information is accurately filled out. Make sure to have your account details on hand to facilitate the process.

Employee Time Card Template - Employers appreciate thorough and accurate timekeeping.

When preparing for a vehicle transfer, it is crucial to understand the significance of the accurate Motor Vehicle Bill of Sale documentation that ensures the legal transfer of ownership between parties in Illinois.

Addendum to Tenancy Agreement - Final terms for security deposits reinforce a protective layer for landlords while balancing tenant rights upon completion of the lease.