Official Loan Agreement Form

Official Loan Agreement Form

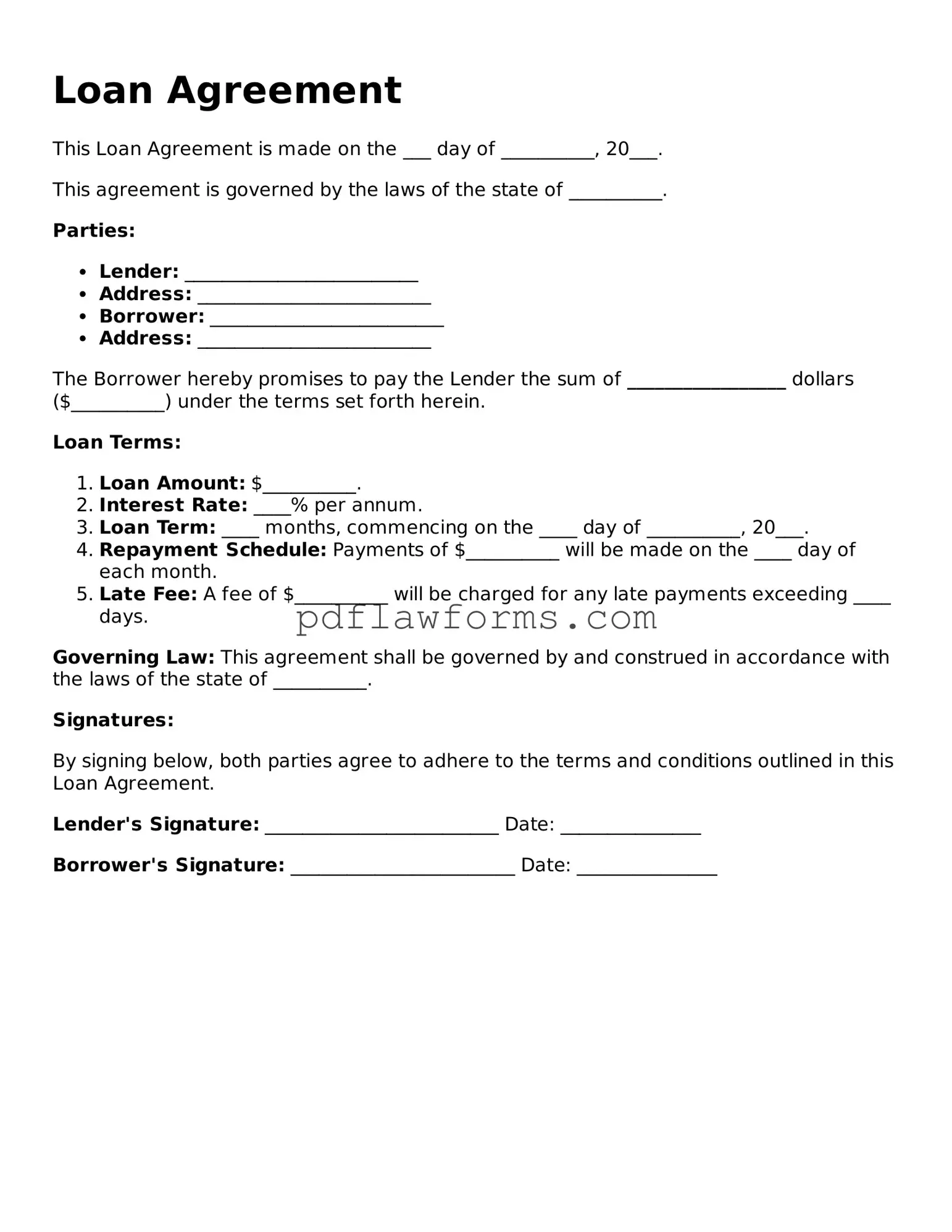

When entering into a financial arrangement, clarity and mutual understanding are crucial. A Loan Agreement form serves as a vital document that outlines the terms and conditions of a loan between a lender and a borrower. It typically includes essential details such as the loan amount, interest rate, repayment schedule, and any collateral involved. Furthermore, the form addresses the rights and responsibilities of both parties, ensuring that expectations are clear from the outset. Provisions regarding default, late fees, and dispute resolution may also be included, providing a framework for what happens if either party fails to meet their obligations. By clearly laying out these aspects, the Loan Agreement form helps to protect the interests of both the lender and the borrower, fostering a sense of security and trust in the transaction.

Understanding loan agreements can be challenging, and several misconceptions often arise. Here are four common misconceptions about loan agreements:

By dispelling these misconceptions, borrowers can approach loan agreements with greater confidence and clarity.

Filling out a Loan Agreement form can be a daunting task, and many individuals make common mistakes that can lead to complications down the line. One prevalent error is not providing complete information. When borrowers leave out important details, such as their full name, address, or Social Security number, it can create confusion and delay the loan process.

Another mistake occurs when individuals fail to read the terms and conditions thoroughly. Skimming through the fine print may seem harmless, but it can lead to misunderstandings about interest rates, repayment schedules, and fees. Borrowers should take the time to understand what they are agreeing to, as this knowledge is crucial for making informed decisions.

Many people also overlook the importance of accurate financial information. Providing incorrect income figures or misrepresenting existing debts can not only jeopardize loan approval but may also have legal implications. It is essential to ensure that all financial data is truthful and up-to-date.

In addition, some borrowers neglect to check for errors in the form itself. Typos or incorrect information can result in processing delays or even rejection of the loan application. A careful review of the entire document before submission can prevent these unnecessary setbacks.

Another common pitfall is misunderstanding the repayment terms. Borrowers may not fully grasp how interest accrues or the implications of late payments. This lack of understanding can lead to financial strain and affect credit scores. It is vital to clarify any uncertainties regarding repayment obligations.

People often forget to include necessary supporting documents as well. Lenders typically require proof of income, identification, and sometimes collateral information. Failing to provide these documents can stall the approval process and create frustration for both parties.

Lastly, some individuals rush through the process without seeking advice. Consulting with a financial advisor or legal expert can provide valuable insights and help avoid costly mistakes. Taking the time to seek guidance can ultimately lead to a smoother loan experience.

Filling out the Loan Agreement form is an important step in securing your loan. Follow these steps carefully to ensure that all necessary information is provided accurately. This will help streamline the process and prevent any delays.

Once you have completed these steps, you can submit the form to the lender. Make sure to keep a copy for your records. This will help you track your loan application and any future communications.

Hurt Feelings Report - A channel through which emotional pain can be shared and potentially resolved.

When considering a California Power of Attorney form, it is essential to familiarize yourself with the various templates available to guide you through the process. Resources such as Templates and Guide can provide valuable assistance in ensuring that you complete the document correctly and according to your specific needs.

Bdsm Limits List - Engage in a healthy exploration of power dynamics through informed choices.