Fill Your IRS 1120 Template

Fill Your IRS 1120 Template

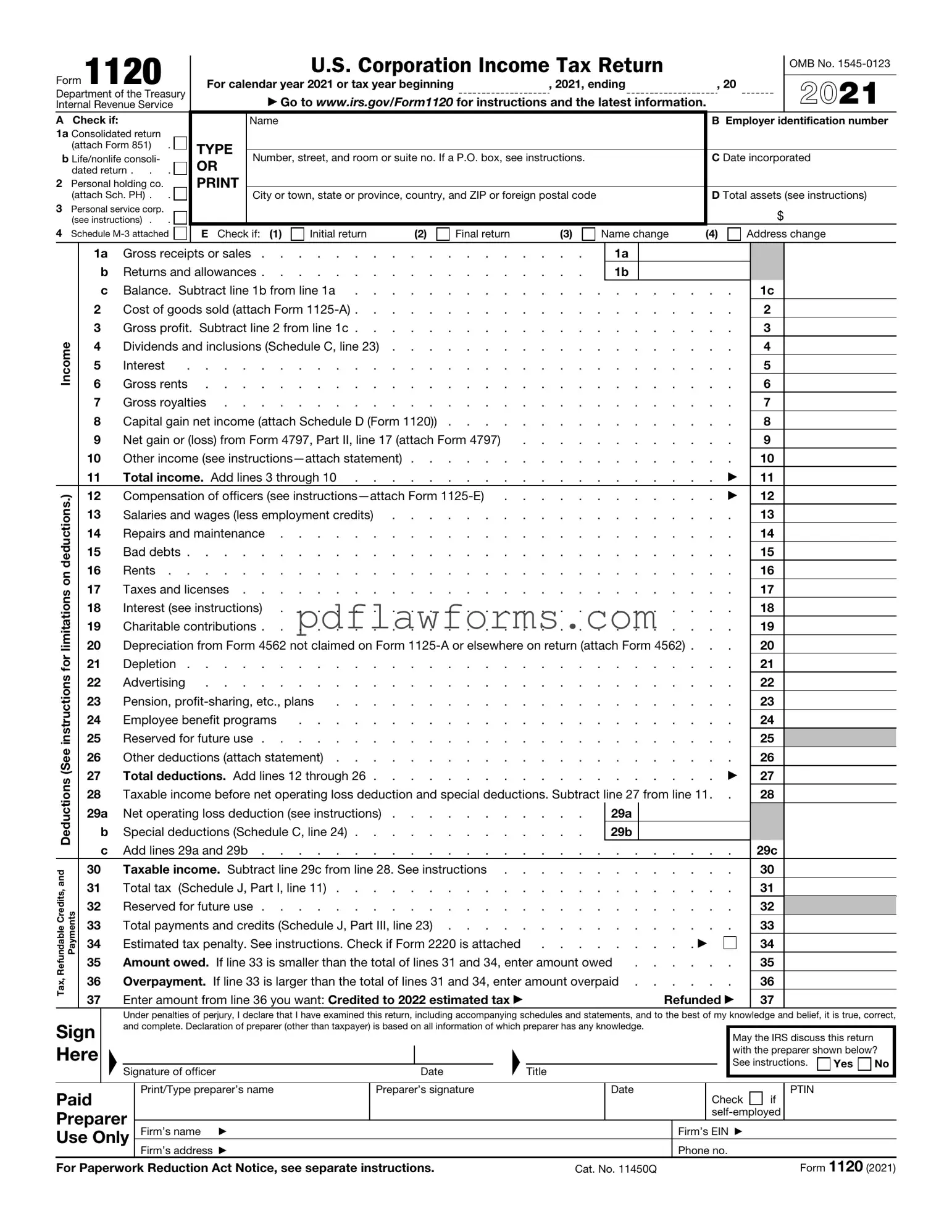

The IRS Form 1120 is a crucial document for corporations operating in the United States, serving as the primary means for reporting income, gains, losses, deductions, and credits to the Internal Revenue Service. This form is essential for C corporations, which are separate legal entities from their owners, and it must be filed annually. Key components of Form 1120 include sections for reporting revenue, calculating taxable income, and detailing the corporation's tax liability. Additionally, corporations must provide information about their deductions, such as business expenses, and any applicable tax credits. The form also requires disclosure of the corporation's total assets and liabilities, which helps the IRS assess the financial health of the business. Filing Form 1120 accurately and on time is vital to avoid penalties and ensure compliance with federal tax laws. Understanding each section of the form is important for corporate officers and accountants alike, as it directly impacts the corporation's tax obligations and overall financial strategy.

The IRS Form 1120 is an important document for corporations in the United States, yet several misconceptions surround its use and requirements. Below is a list of common misunderstandings about this form, along with clarifications to enhance understanding.

Understanding these misconceptions helps corporations navigate their tax responsibilities more effectively. Awareness of the true requirements and implications of Form 1120 can lead to better compliance and financial planning.

Filing the IRS Form 1120 can be a daunting task for many business owners. This form is essential for corporations to report their income, gains, losses, deductions, and credits. However, mistakes are common and can lead to penalties or delayed processing. One frequent error is failing to report all income. It's crucial to include every source of revenue, as the IRS has access to various financial records. Omitting even a small amount can raise red flags and potentially lead to an audit.

Another common mistake is misclassifying expenses. Corporations can deduct certain business expenses, but they must be categorized correctly. For instance, mixing personal and business expenses can result in disallowed deductions. This misclassification not only complicates the filing process but can also lead to an inaccurate tax liability.

Many individuals overlook the importance of accurate calculations. Mathematical errors, whether in totaling income or calculating deductions, can create significant discrepancies. Such mistakes may lead to either overpayment or underpayment of taxes, both of which have consequences. Double-checking calculations or using tax software can help mitigate this risk.

Additionally, failing to sign and date the form is a surprisingly common oversight. A signed form is legally required; without it, the IRS may consider the submission incomplete. This can delay processing and lead to further complications. It’s a simple step, but one that is easily forgotten in the rush to file.

Another issue arises when corporations neglect to keep proper documentation. The IRS requires supporting documents for many deductions claimed on Form 1120. Without adequate records, businesses may struggle to justify their expenses in the event of an audit. Maintaining organized financial records is not just a best practice; it’s essential for compliance.

Finally, many filers fail to be aware of the deadlines. Missing the filing deadline can lead to penalties and interest on unpaid taxes. It’s vital to mark important dates on a calendar and plan ahead to ensure timely submission. Understanding the timeline can save businesses from unnecessary stress and financial burdens.

Completing the IRS Form 1120 is an important step for corporations in the United States to report their income, gains, losses, deductions, and credits. Following the steps outlined below will help ensure that the form is filled out accurately and submitted on time.

Bol Definition - Integrates with electronic systems for improved tracking and management.

In order to facilitate the transfer of ownership and ensure a smooth transaction, it is advisable to utilize resources such as the My PDF Forms which provides templates and guidelines for filling out the Texas RV Bill of Sale form accurately. This helps both the buyer and seller maintain a clear record of the transaction and fulfill legal requirements efficiently.

Cadet Command Forms - The form is prepared as of a specific date, recording the information for tracking purposes.