Promissory Note Form for the State of Illinois

Promissory Note Form for the State of Illinois

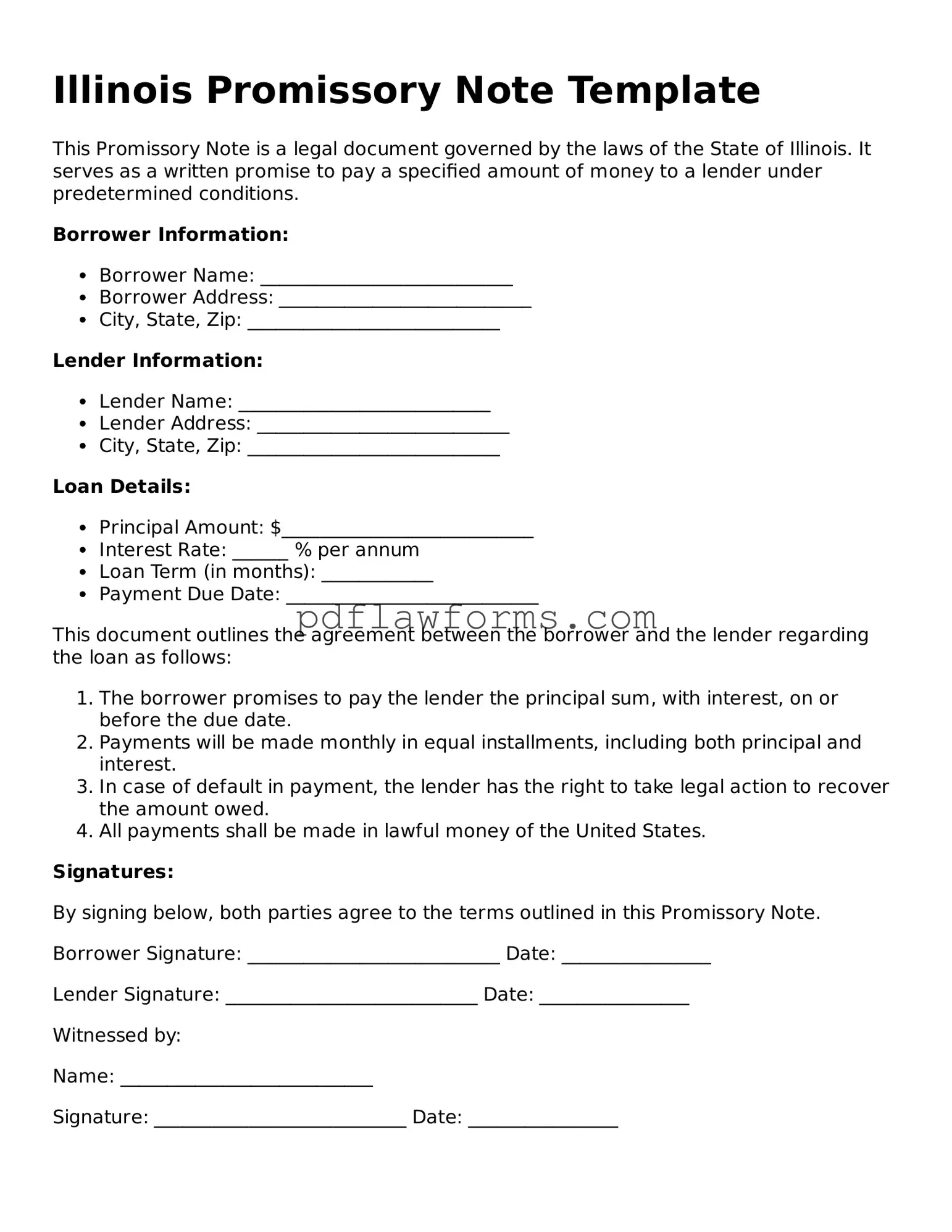

When it comes to borrowing or lending money in Illinois, a Promissory Note is an essential tool that helps establish clear terms and expectations between parties. This written agreement outlines the borrower's promise to repay a specific amount of money to the lender, along with any applicable interest. Key elements of the Illinois Promissory Note include the principal amount, interest rate, repayment schedule, and any late fees that may apply. Additionally, it may specify whether the loan is secured or unsecured, which can significantly affect the lender's rights in case of default. Understanding these components is crucial for both borrowers and lenders, as they ensure that everyone involved knows their obligations and rights. By using this form, individuals can avoid misunderstandings and create a legally binding agreement that protects their interests.

Understanding the Illinois Promissory Note form is crucial for anyone entering into a loan agreement. However, several misconceptions can lead to confusion. Here are six common misconceptions:

Being informed about these misconceptions can help you navigate the complexities of promissory notes more effectively.

When individuals fill out the Illinois Promissory Note form, several common mistakes can lead to complications down the line. One frequent error is failing to include all necessary parties. A promissory note typically requires both a borrower and a lender. Omitting one of these parties can render the document incomplete and unenforceable.

Another common mistake involves incorrect or missing dates. The date of the agreement is crucial, as it establishes when the repayment terms begin. If this date is left blank or inaccurately filled in, it may create confusion regarding the timeline of the loan.

People often overlook the importance of clearly defining the loan amount. Writing the amount in both numeric and written form helps prevent misunderstandings. A mistake in either representation can lead to disputes about how much is actually owed.

Additionally, individuals sometimes neglect to specify the interest rate. If the note does not clearly state whether interest will accrue, it may lead to disagreements later on. Without a defined interest rate, the borrower may not understand their total financial obligation.

Another frequent error is failing to outline the repayment schedule. Whether payments are due monthly, quarterly, or on a different schedule, clarity is essential. A vague repayment structure can create confusion and potential default issues.

People may also forget to include a provision for default. This clause should detail what happens if the borrower fails to make payments. Without this information, the lender may find it challenging to enforce their rights if the borrower defaults.

Many individuals do not sign the document in the appropriate places. Both parties should sign the note to validate it. A missing signature can lead to questions about the authenticity of the agreement.

In some cases, individuals fail to have the document notarized. While notarization is not always required, having a notary public witness the signatures can add an extra layer of legitimacy to the note.

People often overlook the need for clear contact information. Including addresses and phone numbers for both parties ensures that communication can occur if issues arise. Without this information, resolving disputes may become more complicated.

Finally, individuals sometimes do not keep a copy of the signed note for their records. Retaining a copy is essential for both parties to have proof of the agreement. Without this documentation, enforcing the terms may become difficult.

Once you have the Illinois Promissory Note form ready, it’s time to fill it out accurately. This document serves as a written promise to repay a loan, so clarity is essential. Follow these steps to ensure you complete the form correctly.

After completing the form, make copies for both the borrower and lender. This ensures that both parties have a record of the agreement. It's also wise to keep the original in a safe place.

Promissory Note Template Florida - Templates for promissory notes are often available for individuals and businesses to use.

Promissory Note Download - Many financial institutions use standardized language in promissory notes for consistency.

Free Promissory Note Template Georgia - Late fees may be outlined in the note to encourage timely payments.

When engaging in a transaction involving a recreational vehicle, it is essential to utilize the Texas RV Bill of Sale, as it formally records ownership transfer and clarifies both parties' responsibilities. For those looking for a reliable source to obtain this document, you can visit My PDF Forms to ensure a smooth process.

Promissory Note Form California - A promissory note is an important tool for managing personal or business finances.