Fill Your Gift Letter Template

Fill Your Gift Letter Template

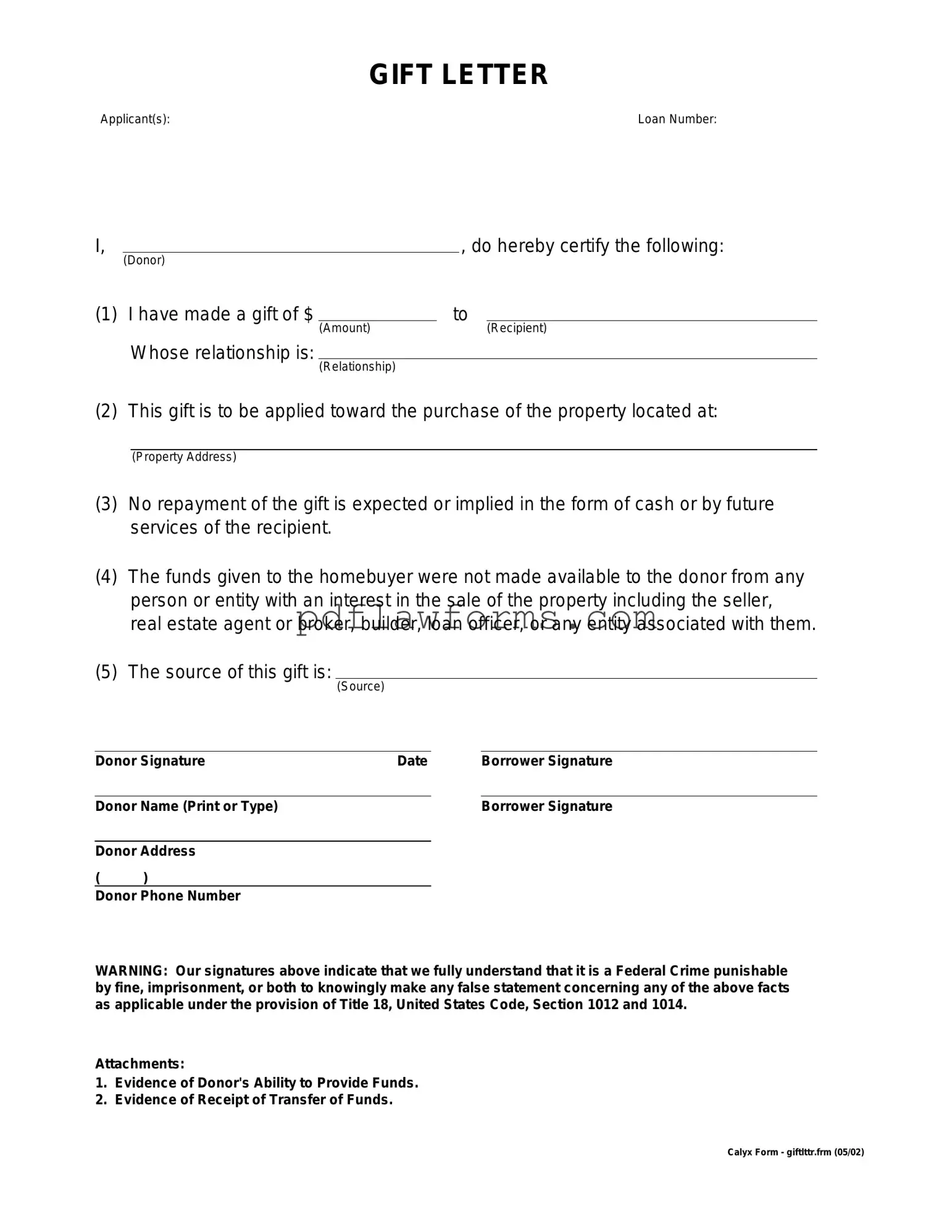

The Gift Letter form plays a crucial role in the process of securing financing for a home. This document is often required by lenders when a borrower receives funds as a gift from family or friends to help with a down payment or closing costs. It serves to clarify the source of the funds and ensures that the money is indeed a gift, not a loan that needs to be repaid. Typically, the form includes essential details such as the donor's name, relationship to the borrower, the amount of the gift, and a statement confirming that the funds do not need to be repaid. By providing this information, the Gift Letter helps lenders assess the borrower’s financial situation more accurately. Additionally, it protects both the borrower and the donor by documenting the transaction. Overall, understanding the Gift Letter form is vital for anyone looking to navigate the home-buying process with financial assistance from loved ones.

Gift letters are important documents in real estate transactions, particularly when it comes to securing a mortgage. However, several misconceptions can lead to confusion. Here are eight common misconceptions about the Gift Letter form, along with explanations to clarify them.

Many believe that gift letters are only necessary when the financial gift exceeds a certain threshold. In reality, lenders often require a gift letter regardless of the amount to ensure compliance with their policies.

While gifts can be made by anyone, lenders typically prefer that gifts come from family members. This helps establish the legitimacy of the funds and reduces the risk of fraud.

This misconception can lead to serious issues. A gift letter explicitly states that the funds are a gift, not a loan, which means the recipient is not required to repay the money.

While notarization is not always required, some lenders may ask for it to verify the authenticity of the gift letter. It is best to check with the lender for their specific requirements.

Verbal agreements are not sufficient. A written gift letter is essential for documentation purposes and must include specific information about the gift and the giver.

Gift letters can be used by anyone purchasing a home, not just first-time buyers. They are a common tool for buyers seeking financial assistance from family members.

While it is best to have accurate information from the start, if changes are necessary, a new gift letter can be drafted and signed to reflect the updated details.

Even if the gifted funds are already in the recipient's bank account, a gift letter may still be required to clarify the source of the funds and confirm that they are a gift.

Understanding these misconceptions can help individuals navigate the gift letter process more effectively. It is always advisable to consult with a lender or financial advisor for guidance tailored to specific situations.

When filling out a Gift Letter form, individuals often overlook key details that can lead to complications later on. One common mistake is failing to provide complete information about the donor. The donor's full name, address, and relationship to the recipient should be clearly stated. Omitting any of this information can raise questions about the legitimacy of the gift, potentially complicating tax implications or loan approvals.

Another frequent error involves not specifying the amount of the gift. It is essential to clearly indicate the exact dollar amount being gifted. If this information is left vague or incomplete, it may lead to misunderstandings or disputes regarding the gift's value. This can be particularly problematic in financial transactions, such as applying for a mortgage, where lenders require precise figures.

People also sometimes neglect to include a statement confirming that the gift does not need to be repaid. This affirmation is crucial to clarify the nature of the transaction. Without this statement, the recipient may face scrutiny regarding whether the funds are a loan rather than a gift. Such confusion can create unnecessary complications in both personal and financial matters.

Finally, a common oversight is failing to sign and date the form. Both the donor and recipient should ensure that their signatures are present, along with the date of the transaction. A missing signature can render the Gift Letter invalid, leading to potential issues down the line. Proper completion of the form is vital for ensuring that all parties involved are protected and that the gift is recognized as intended.

Filling out a Gift Letter form is an important step in documenting a financial gift, especially when it relates to significant transactions like home purchases. After completing this form, it will serve as a formal declaration of the gift, ensuring that all parties involved understand the nature of the funds provided.

Florida Realtor Forms - The contract specifies the purchase price and details about deposits.

Direction to Pay - Taking the time to fill out this form properly can save time and stress during the repair process.

A California Lease Agreement form is a vital document that defines the relationship between landlords and tenants, ensuring clarity and fairness throughout the rental process. For those seeking assistance with drafting this important contract, various resources are available, including helpful templates such as the one found at Templates and Guide, which can simplify the creation of a comprehensive agreement.

How to Write a Continuance Letter for Court - Submitting this motion does not guarantee a new hearing date.