Loan Agreement Form for the State of Georgia

Loan Agreement Form for the State of Georgia

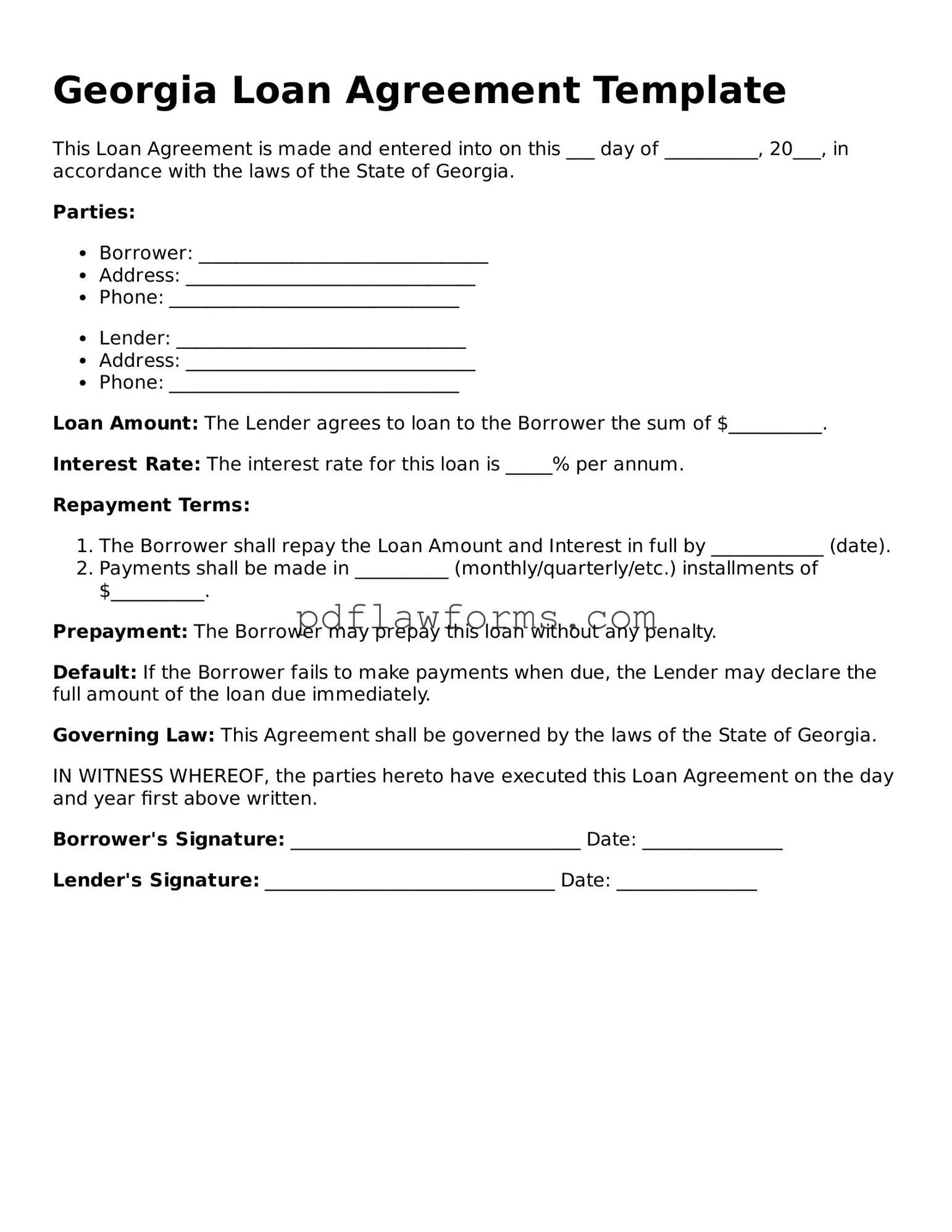

The Georgia Loan Agreement form serves as a crucial document for individuals and businesses engaging in lending transactions within the state. This form outlines the terms and conditions under which a borrower agrees to repay the loan to the lender. Key aspects of the agreement include the principal amount borrowed, the interest rate, repayment schedule, and any applicable fees. Additionally, it specifies the rights and responsibilities of both parties, ensuring clarity and protection throughout the loan process. The form may also address default provisions, which outline the consequences if the borrower fails to make timely payments. Understanding the components of the Georgia Loan Agreement is essential for both lenders and borrowers to navigate their financial commitments effectively and to foster a transparent lending relationship.

Many people have misunderstandings about the Georgia Loan Agreement form. Here are some common misconceptions, along with explanations to clarify them.

Understanding these misconceptions can help ensure that both borrowers and lenders are well-informed when using the Georgia Loan Agreement form.

Filling out a Georgia Loan Agreement form can be a straightforward process, but many individuals make common mistakes that can lead to complications down the line. One of the most frequent errors is failing to read the instructions carefully. Each section of the form is designed to gather specific information. Skipping over these details may result in incomplete or inaccurate submissions.

Another common mistake is not providing accurate personal information. This includes your name, address, and contact details. Even a small typo can lead to confusion or delays in processing your loan. Always double-check this information to ensure it is correct.

Many people overlook the importance of understanding the terms of the loan. It’s crucial to grasp the interest rate, repayment schedule, and any fees associated with the loan. Ignoring these details can lead to unexpected financial burdens later on. Take the time to read through the terms and ask questions if something is unclear.

In addition, individuals sometimes forget to sign and date the form. A signature is a critical part of the agreement, as it signifies your acceptance of the terms. Without it, the document may be considered invalid. Ensure that you sign in the designated area and include the date.

Another mistake is not providing supporting documentation when required. Lenders often ask for proof of income, identification, or other financial documents to verify your eligibility. Failing to include these can slow down the approval process or even result in denial.

Some borrowers neglect to keep a copy of the completed agreement for their records. This can be problematic if there are disputes or if you need to refer back to the terms in the future. Always retain a copy for your personal files.

Additionally, individuals may fail to disclose all debts or financial obligations. Being transparent about your financial situation is essential for lenders to assess your ability to repay the loan. Omitting information can lead to complications later on, including potential legal issues.

Another frequent oversight involves misunderstanding the repayment terms. Some borrowers may not realize that missing a payment can have serious consequences. Familiarize yourself with the repayment schedule and plan accordingly to avoid any pitfalls.

Finally, many individuals rush through the process without seeking assistance when needed. If you find yourself confused or uncertain about any part of the form, don’t hesitate to ask for help. It’s better to take a little extra time to ensure everything is correct than to face issues later.

Completing the Georgia Loan Agreement form is an important step in securing a loan. This process involves providing accurate information and ensuring that all necessary details are included. Once the form is filled out correctly, it can be submitted to the lender for review and approval.

Promissory Note Florida Pdf - Borrowers commit to repay the loan under specified terms agreed upon by both parties.

Free Promissory Note Template California - The agreement may also outline the circumstances under which the loan can be called due.

When engaging in a vehicle transaction in Florida, it's important to ensure all details are documented thoroughly; the Florida Motor Vehicle Bill of Sale form, which can be found at floridaformspdf.com/printable-motor-vehicle-bill-of-sale-form/, encapsulates necessary information about the vehicle, including its description and purchase price, thereby facilitating a smooth ownership transfer process.

Promissory Note Template Illinois - The document often includes provisions for early repayment or refinancing options.