Deed in Lieu of Foreclosure Form for the State of Georgia

Deed in Lieu of Foreclosure Form for the State of Georgia

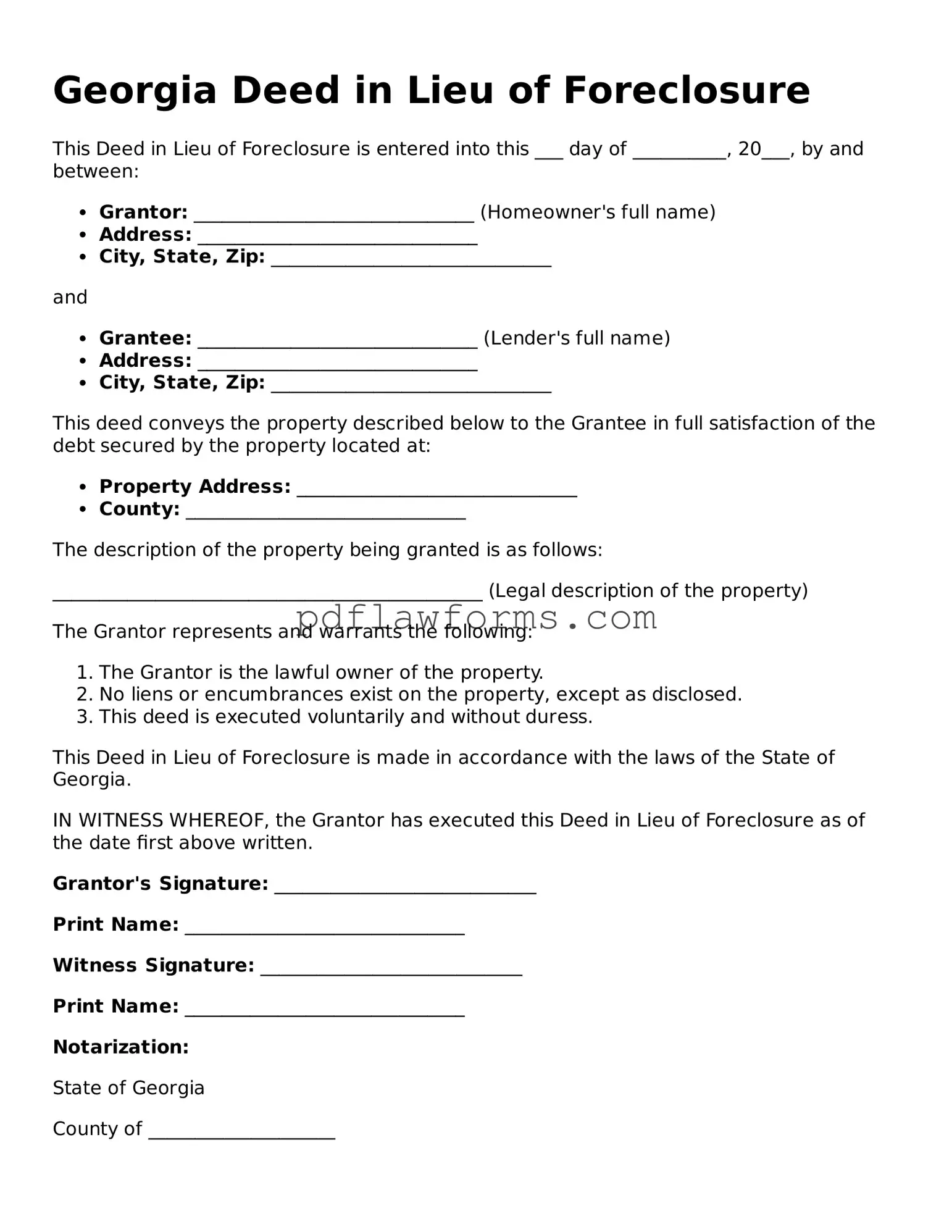

In Georgia, the Deed in Lieu of Foreclosure form serves as a crucial tool for homeowners facing financial difficulties. This option allows property owners to voluntarily transfer their property back to the lender, effectively avoiding the lengthy and often stressful foreclosure process. By completing this form, homeowners can potentially mitigate the impact on their credit score and find a quicker resolution to their mortgage challenges. The process typically involves the homeowner providing a clear title to the property, which the lender then accepts in exchange for releasing the homeowner from their mortgage obligations. This arrangement can be beneficial for both parties, as it helps the lender recover the property while offering the homeowner a chance to move forward without the burden of foreclosure. Understanding the key components of this form is essential for anyone considering this path, as it outlines the rights and responsibilities of both the homeowner and the lender, ensuring that the transition is as smooth as possible.

Understanding the Georgia Deed in Lieu of Foreclosure form can be challenging, leading to several misconceptions. Here are nine common misunderstandings about this important legal document:

Being informed about these misconceptions can help homeowners make better decisions when facing financial difficulties. Understanding the true nature of a deed in lieu of foreclosure is essential for navigating the complexities of real estate and mortgage challenges.

When filling out the Georgia Deed in Lieu of Foreclosure form, many people inadvertently make mistakes that can complicate the process. One common error is failing to provide accurate property information. It’s essential to include the correct legal description of the property, as any discrepancies can lead to delays or even rejection of the deed. Double-checking this information can save time and frustration later on.

Another mistake involves not obtaining the necessary signatures. All parties involved in the transaction must sign the deed, including any co-owners. If a required signature is missing, the deed may not be valid. It’s wise to ensure that everyone who has a stake in the property is present and ready to sign before submitting the form.

People often overlook the importance of notarization. In Georgia, a Deed in Lieu of Foreclosure must be notarized to be legally binding. Failing to have the document notarized can render it ineffective. It’s a simple step, but one that is frequently forgotten.

Another common error is not including a clear statement of intent. The form should clearly indicate that the borrower is voluntarily transferring the property to the lender to avoid foreclosure. Without this clarity, the lender may have difficulty processing the deed, leading to further complications.

Additionally, many individuals fail to understand the implications of the deed. Some mistakenly believe that a deed in lieu of foreclosure is the same as a short sale. While both options can help avoid foreclosure, they have different consequences. Understanding these differences can help homeowners make more informed decisions.

People sometimes neglect to consult with a legal professional. While it may seem straightforward, the process can be complex, and having legal guidance can help navigate potential pitfalls. An attorney can provide valuable insights and ensure that all necessary steps are taken correctly.

Furthermore, individuals may not consider the tax implications of transferring the property. In some cases, the IRS may view the forgiven debt as taxable income. It’s crucial to be aware of these potential tax consequences and plan accordingly.

Lastly, not keeping copies of the completed form can lead to issues down the line. Always retain a copy of the signed deed for personal records. This documentation can be essential if any questions arise in the future regarding the transfer of ownership.

After completing the Georgia Deed in Lieu of Foreclosure form, the next step involves submitting the document to the appropriate parties, which may include your lender and local county office. Ensure that you keep copies for your records and confirm receipt with the lender.

The Loan Servicer Might Agree to Put the Foreclosure on Hold to Give You Some Time to Sell Your Home - Lenders may prefer this option to reduce their holding costs on properties.

Will I Owe Money After a Deed in Lieu of Foreclosure - Homeowners who complete this process often find it less complicated than navigating foreclosure.

California Property Transfer Deed - This deed simplifies the process by directly transferring the title of the property to the lender.

To facilitate the management of a motor vehicle in Florida, individuals may utilize the Florida Motor Vehicle Power of Attorney form, which grants authority to another person to handle transactions such as buying, selling, or registering the vehicle. This legal document is essential for ensuring that all vehicle-related tasks are taken care of, even when the owner is unavailable. For those interested, a comprehensive resource can be found at https://floridaformspdf.com/printable-motor-vehicle-power-of-attorney-form.

Deed in Lieu of Foreclosure Template - This form allows the borrower to smoothly transition out of homeownership if they can no longer manage the property.