Loan Agreement Form for the State of Florida

Loan Agreement Form for the State of Florida

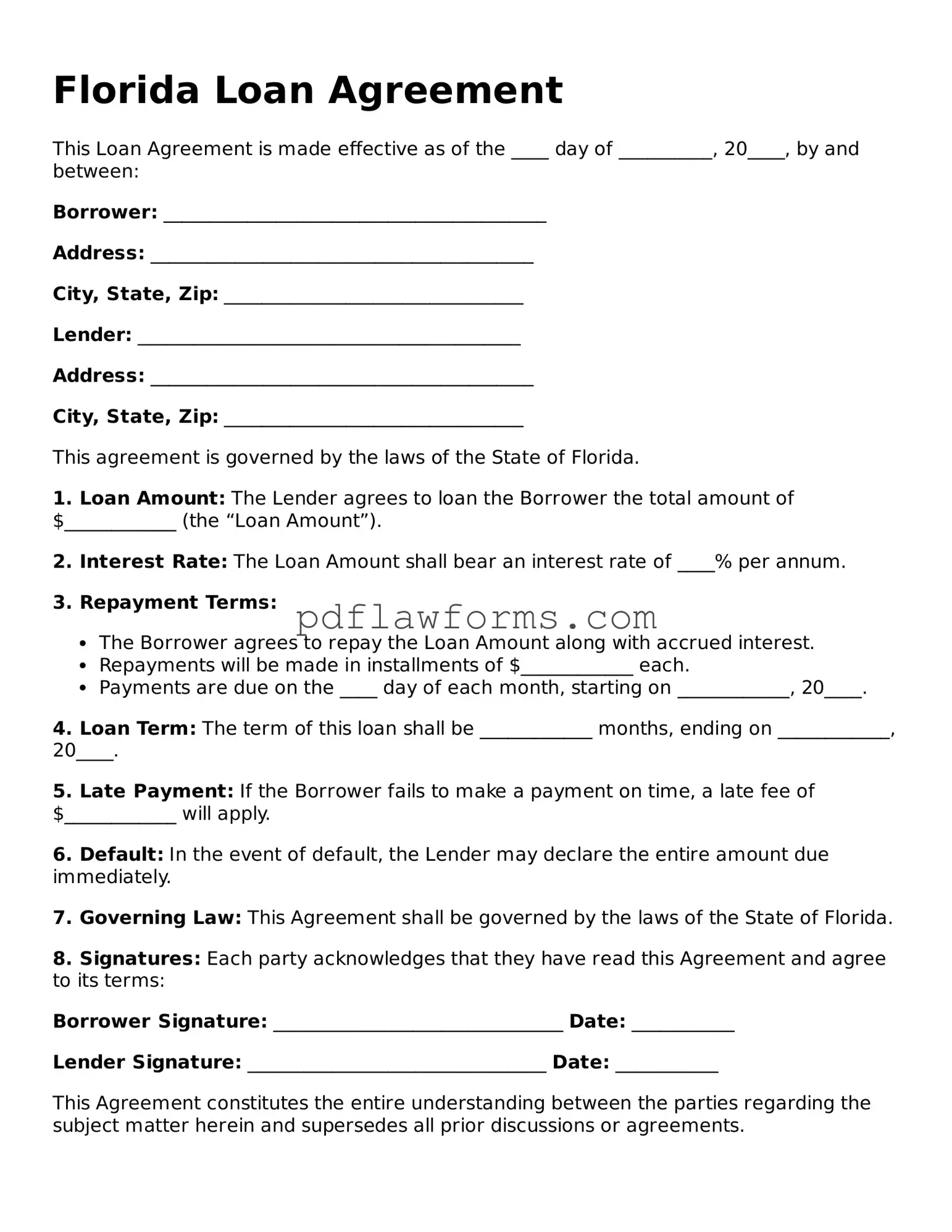

In the state of Florida, the Loan Agreement form serves as a crucial document that outlines the terms and conditions of a loan between a lender and a borrower. This form typically includes essential details such as the loan amount, interest rate, repayment schedule, and any collateral required to secure the loan. Additionally, it specifies the rights and responsibilities of both parties, ensuring clarity and legal protection. The agreement may also address default scenarios, outlining the steps that can be taken if the borrower fails to meet repayment obligations. By providing a structured framework for the loan transaction, the Florida Loan Agreement form helps to mitigate risks and foster trust between the lender and borrower. Understanding the components of this form is vital for anyone involved in lending or borrowing in Florida, as it lays the groundwork for a successful financial arrangement.

Understanding the Florida Loan Agreement form can be challenging, especially with the many misconceptions surrounding it. Here are ten common misunderstandings, along with clarifications to help you navigate this important document.

Many people believe that all loan agreements follow a standard format. In reality, each loan agreement can vary significantly based on the lender, the type of loan, and specific terms negotiated between the parties.

Some individuals think they can simply sign the document without reviewing it. However, it’s crucial to read and understand all terms and conditions to avoid unexpected obligations.

It’s a common belief that only the lender's signature is necessary. In fact, both parties must sign the agreement to make it legally binding.

Some people think that loan agreements are informal and not enforceable. In reality, a properly executed loan agreement is a legally binding contract that can be upheld in court.

Many believe that a verbal agreement is enough. However, having a written loan agreement is essential for clarity and legal protection.

Some assume that every loan must be secured with collateral. While many loans do require collateral, unsecured loans exist as well.

It’s a misconception that all loan agreements have fixed interest rates. Some loans feature variable rates that can change over time based on market conditions.

Many people think that loan agreements are only necessary for significant sums of money. However, even smaller loans can benefit from a formal agreement to clarify terms.

Some believe that a signed loan agreement cannot be altered. In truth, parties can amend the agreement if both agree to the changes in writing.

It’s a common misunderstanding that loan agreements apply only to personal loans. They can also be used for business loans, mortgages, and other financial transactions.

By addressing these misconceptions, you can approach the Florida Loan Agreement form with greater confidence and understanding.

Filling out the Florida Loan Agreement form can be a straightforward process, but mistakes often occur. One common error is failing to provide accurate personal information. When individuals do not double-check their names, addresses, or Social Security numbers, it can lead to complications later on. Ensuring that all personal details are correct is essential for the validity of the agreement.

Another frequent mistake is neglecting to specify the loan amount clearly. If the amount is ambiguous or incorrectly stated, it can create confusion and disputes between the lender and borrower. It is crucial to write the loan amount in both numerical and written form to avoid any misunderstandings.

People sometimes overlook the importance of detailing the repayment terms. This includes the interest rate, payment schedule, and any penalties for late payments. A lack of clarity in these areas can lead to disagreements down the line. Clearly outlining these terms helps protect both parties and sets clear expectations.

Additionally, individuals may fail to sign the document properly. Signatures are vital for the agreement's enforceability. If a signature is missing or not dated, it can render the agreement void. Always ensure that all required parties sign and date the form correctly.

Another mistake involves not including any necessary disclosures. Florida law requires certain disclosures to be made in loan agreements. Failing to include these can result in legal issues. It is important to be aware of what disclosures are required and to include them in the agreement.

Some borrowers also make the mistake of not reading the entire agreement before signing. This can lead to misunderstandings about the terms and conditions. Taking the time to review the document thoroughly can prevent future problems and ensure that all parties are on the same page.

Lastly, individuals may not keep a copy of the signed agreement. Having a copy is essential for personal records and can be important if any disputes arise. Always make sure to retain a signed copy for future reference.

After obtaining the Florida Loan Agreement form, you will need to complete it accurately to ensure that all parties involved understand the terms of the loan. This process involves providing specific information about the loan, the borrower, and the lender. Follow these steps carefully to fill out the form correctly.

Once you have completed the form, review it for accuracy before sharing it with the other party. This step is crucial for ensuring that everyone is on the same page regarding the terms of the loan.

Free Promissory Note Template California - The form defines the loan amount and any applicable fees associated with the loan.

The USCIS I-864 form, also known as the Affidavit of Support, is a crucial document required for certain immigration processes in the United States. This form ensures that immigrant applicants have adequate financial support and are not likely to become a public charge. By filling out this form, sponsors demonstrate their commitment to financially support the immigrant for a specified period. For more information, you may visit My PDF Forms.