Deed in Lieu of Foreclosure Form for the State of Florida

Deed in Lieu of Foreclosure Form for the State of Florida

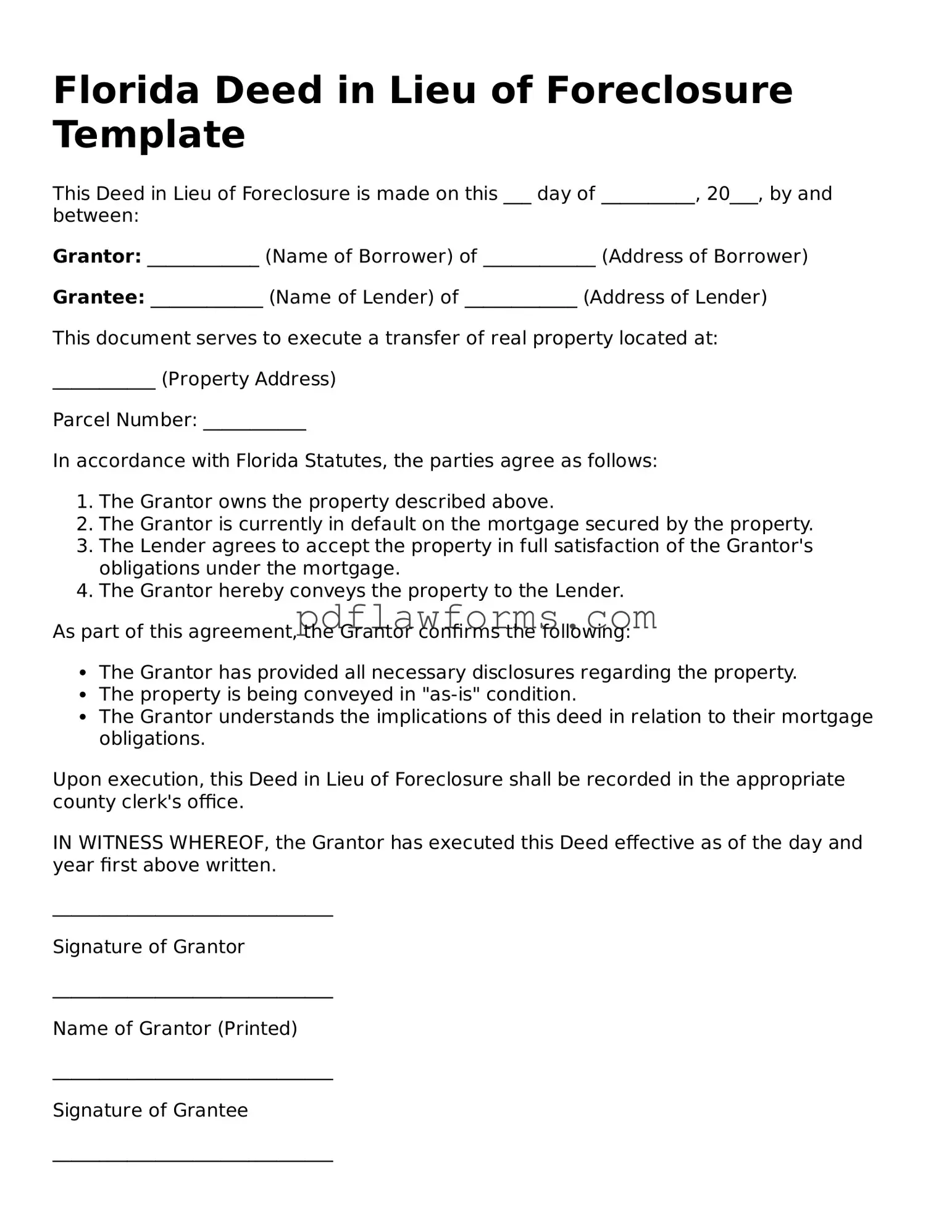

In the face of financial hardship, homeowners in Florida often seek alternatives to foreclosure, one of which is the Deed in Lieu of Foreclosure. This legal instrument allows a borrower to voluntarily transfer ownership of their property back to the lender, effectively relinquishing their rights to the home in exchange for the cancellation of the mortgage debt. The process typically involves a series of steps, including the completion of the Deed in Lieu of Foreclosure form, which outlines the terms of the transfer and ensures that both parties understand their rights and obligations. Importantly, this form serves to protect the lender's interests while offering the borrower a potential path to avoid the long-term consequences of foreclosure. Additionally, the form may include clauses addressing issues such as deficiency judgments, which can arise when the property value is less than the outstanding mortgage balance. By understanding the intricacies of this form, homeowners can make informed decisions that may alleviate their financial burdens and facilitate a smoother transition away from homeownership.

Understanding the Florida Deed in Lieu of Foreclosure form is crucial for homeowners facing financial difficulties. However, several misconceptions can lead to confusion. Here are six common misconceptions:

Addressing these misconceptions can help homeowners make informed decisions regarding their financial situation and the potential use of a deed in lieu of foreclosure.

When homeowners face the daunting prospect of foreclosure, a Deed in Lieu of Foreclosure can sometimes offer a viable alternative. However, filling out this form is not as straightforward as it may seem. Many people make mistakes that can complicate the process or even render the deed ineffective. Here are nine common pitfalls to avoid.

First, one of the most frequent errors is failing to understand the terms of the deed itself. A Deed in Lieu of Foreclosure transfers ownership of the property back to the lender, but it also comes with specific obligations. Homeowners often overlook the implications of this transfer, including potential tax consequences. Understanding these terms is crucial before signing any documents.

Another common mistake is not including all necessary parties in the deed. If the property is jointly owned, all owners must sign the document. Omitting a co-owner can lead to legal complications later on. Ensuring that every individual with an interest in the property is accounted for is essential to avoid future disputes.

Some homeowners also neglect to provide accurate property descriptions. The deed must include a clear and precise description of the property being transferred. Inaccuracies can cause confusion and may delay the process. It's important to double-check this information against official records to ensure it is correct.

Additionally, many individuals fail to seek legal advice before completing the deed. While it may seem like a straightforward process, the implications of a Deed in Lieu of Foreclosure can be significant. Consulting with a legal professional can help clarify any uncertainties and ensure that the homeowner's rights are protected.

In some cases, homeowners do not fully disclose all liens or encumbrances on the property. The lender needs to be aware of any existing debts associated with the property. Failing to disclose this information can lead to complications and may even result in the lender refusing the deed.

Another mistake involves overlooking the importance of notarization. Many people assume that simply signing the document is enough. However, a notary public must witness the signing for the deed to be legally binding. Skipping this step can invalidate the entire process.

Homeowners may also forget to retain copies of the completed deed and any related correspondence. Keeping thorough records is vital, as it provides proof of the transaction and can be useful if disputes arise later. Documenting every step of the process helps ensure clarity and accountability.

Moreover, some individuals rush through the process without fully understanding the lender's requirements. Each lender may have different criteria for accepting a Deed in Lieu of Foreclosure. Homeowners should take the time to review these requirements carefully to avoid unnecessary delays or rejections.

Finally, failing to communicate effectively with the lender can lead to misunderstandings. Clear and open communication is key throughout the process. Homeowners should ensure they understand the lender’s expectations and keep them informed of any changes in their situation.

By being aware of these common mistakes, homeowners can navigate the Deed in Lieu of Foreclosure process more effectively. Taking the time to understand the requirements and implications can lead to a smoother transition and a better outcome.

Once you have decided to proceed with the Deed in Lieu of Foreclosure, it is essential to complete the necessary form accurately. This step is crucial as it can significantly impact your financial future and property ownership status. Make sure to gather all required information before you begin filling out the form.

After submitting the form, the lender will review it and may contact you for further information. It is crucial to stay in communication with them throughout this process to ensure a smooth transition. Be prepared for any additional steps that may arise as you move forward.

Will I Owe Money After a Deed in Lieu of Foreclosure - Filing a Deed in Lieu of Foreclosure can be a proactive step for individuals unable to keep their home.

The Loan Servicer Might Agree to Put the Foreclosure on Hold to Give You Some Time to Sell Your Home - Both parties need to clearly outline responsibilities regarding property condition.

This Hold Harmless Agreement plays a vital role in protecting individuals and businesses during transactions. By utilizing this form, you can ensure your interests are safeguarded. For further details and to access this necessary document, check out the complete information regarding the Hold Harmless Agreement form to protect your assets effectively.

California Property Transfer Deed - Lenders typically prefer this solution as it can save them time and expenses associated with foreclosure.”