Official Deed in Lieu of Foreclosure Form

Official Deed in Lieu of Foreclosure Form

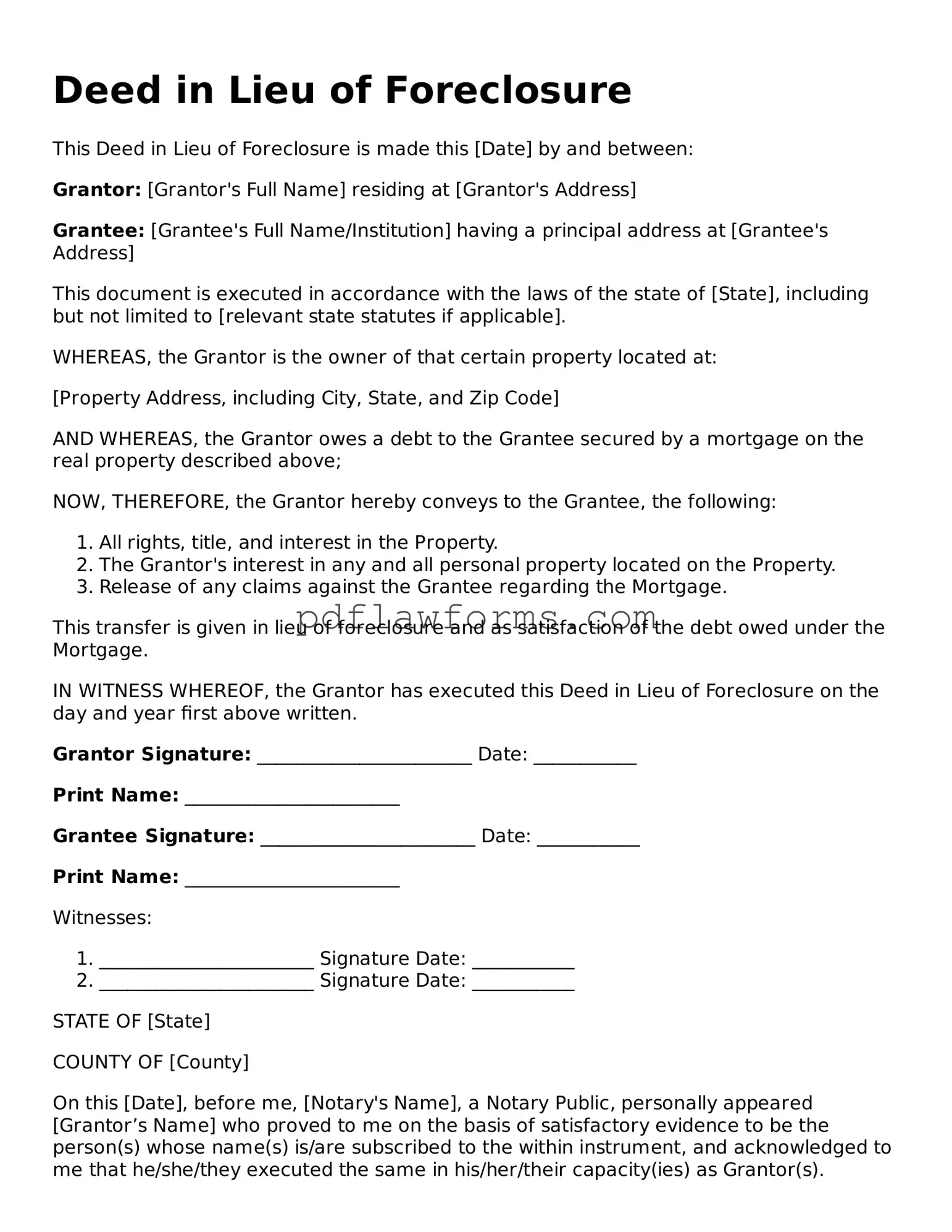

The Deed in Lieu of Foreclosure form serves as a significant tool for homeowners facing financial difficulties and potential foreclosure. This legal document allows a property owner to voluntarily transfer ownership of their property back to the lender, effectively avoiding the lengthy and often costly foreclosure process. By executing this form, homeowners can mitigate the adverse effects of foreclosure on their credit scores and overall financial health. The process typically involves negotiations between the homeowner and the lender, ensuring that both parties understand the implications of the deed transfer. Additionally, the form may include provisions that address any outstanding debts associated with the mortgage, as well as stipulations regarding the condition of the property upon transfer. It is crucial for homeowners to comprehend the benefits and potential drawbacks of this option, as it may impact their future borrowing capabilities and financial landscape. Understanding the nuances of the Deed in Lieu of Foreclosure form can empower homeowners to make informed decisions in challenging circumstances.

A Deed in Lieu of Foreclosure is a legal option for homeowners facing foreclosure. However, several misconceptions surround this process. Below are four common misunderstandings:

Many believe that signing a Deed in Lieu of Foreclosure automatically cancels any remaining mortgage debt. In reality, while this process can relieve the homeowner of the property, it does not always absolve them of all financial obligations. Lenders may still pursue deficiency judgments for any remaining balance.

Some homeowners think that a Deed in Lieu of Foreclosure will expedite the process of leaving their home. However, this option can involve lengthy negotiations with the lender. The timeline can vary significantly based on the lender's policies and the specific circumstances of the case.

While the concept may seem simple, the actual process can be complex. Homeowners must meet specific criteria set by the lender, and documentation can be extensive. It is crucial to understand the requirements and implications before proceeding.

Another misconception is that a Deed in Lieu of Foreclosure has no impact on credit scores. In fact, this action is likely to negatively affect credit ratings, similar to a foreclosure. The long-term financial consequences can be significant.

Filling out a Deed in Lieu of Foreclosure form requires careful attention to detail. One common mistake is providing inaccurate property information. It is crucial to ensure that the address and legal description of the property are correct. Errors in this section can lead to complications in the future.

Another frequent error involves not including all necessary parties. All owners of the property must sign the deed. Omitting a co-owner can invalidate the document, causing delays and potential legal issues.

Many individuals overlook the importance of obtaining the lender's approval before submitting the deed. A Deed in Lieu of Foreclosure should not be executed without the lender's consent. Failing to do so may result in unexpected consequences, including continued liability for the mortgage.

Some people neglect to seek legal advice when completing the form. While it may seem straightforward, the implications of a Deed in Lieu of Foreclosure can be significant. Consulting with a legal professional can provide clarity and help avoid costly mistakes.

Additionally, individuals sometimes forget to include a statement of intent. Clearly stating the purpose of the deed can help prevent misunderstandings. This statement can clarify that the transfer is voluntary and intended to satisfy the mortgage obligation.

It is also common for individuals to skip the notarization process. A Deed in Lieu of Foreclosure typically requires notarization to be legally binding. Failing to have the document notarized can render it ineffective.

Another mistake is not retaining a copy of the completed form. Keeping a record of all submitted documents is essential for future reference. This can be helpful if any disputes arise after the transfer.

Many individuals do not fully understand the tax implications of executing a Deed in Lieu of Foreclosure. It is important to consult with a tax professional to understand potential consequences. This oversight can lead to unexpected financial burdens.

Lastly, some people rush through the process without reviewing the document thoroughly. Taking the time to read and understand the form can prevent errors. A careful review ensures that all information is accurate and complete.

After completing the Deed in Lieu of Foreclosure form, you will need to submit it to your lender. They will review the document and determine the next steps. It is important to keep communication open with your lender during this process.

Title Companies and Transfer on Death Deeds - If you have no current heirs or wish to exclude certain people from inheritance, a Transfer-on-Death Deed helps clarify your desires.

The California Employment Verification form is a document used to confirm an individual's employment history and status. This form plays a crucial role in various processes, such as background checks and loan applications. For those seeking further assistance, resources like Templates and Guide can provide invaluable support in understanding how to properly complete and use this form, streamlining many necessary verifications in both personal and professional scenarios.