Fill Your Cg 20 10 07 04 Liability Endorsement Template

Fill Your Cg 20 10 07 04 Liability Endorsement Template

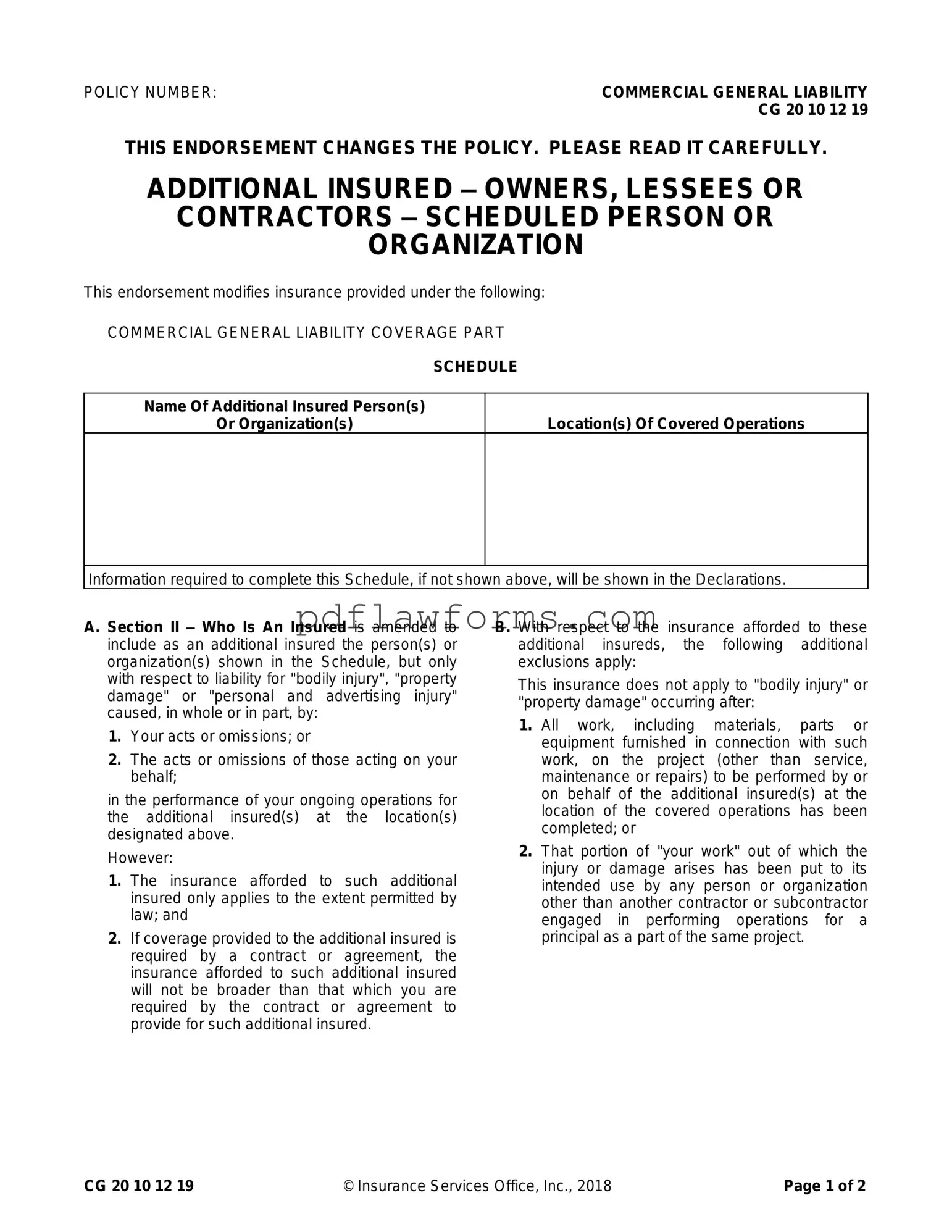

The CG 20 10 07 04 Liability Endorsement form is an important document within the realm of commercial general liability insurance. It serves to extend coverage to additional insured parties, such as owners, lessees, or contractors, who may have a vested interest in the operations being conducted. This endorsement specifically outlines the circumstances under which these additional insureds are covered, particularly regarding liability for bodily injury, property damage, or personal and advertising injury. The form stipulates that coverage applies only when the injury or damage arises from the actions of the insured or those acting on their behalf during ongoing operations at designated locations. Importantly, the coverage is limited to what is permitted by law and cannot exceed the terms specified in any underlying contracts or agreements. Additionally, the endorsement introduces exclusions, particularly regarding work that has been completed or when the insured's work has been put to its intended use by others. Furthermore, it clarifies that the limits of insurance for these additional insureds will not exceed what is required by contract or the available policy limits. Understanding this endorsement is crucial for businesses and contractors as it can significantly impact their liability coverage and obligations under various agreements.

Misconceptions about the CG 20 10 07 04 Liability Endorsement form can lead to misunderstandings regarding coverage and responsibilities. Here are nine common misconceptions:

Understanding these misconceptions can help clarify the coverage provided by the CG 20 10 07 04 Liability Endorsement and ensure that all parties are aware of their rights and responsibilities.

Filling out the CG 20 10 07 04 Liability Endorsement form can be a straightforward process, but mistakes are common. One significant error occurs when individuals fail to include the correct policy number. This number is essential for identifying the specific insurance policy in question. Omitting or miswriting this number can lead to delays or denials of coverage when it is needed most.

Another frequent mistake involves neglecting to list all required additional insured parties. It is crucial to accurately identify each person or organization that needs to be covered under the endorsement. Leaving out an additional insured can expose both the primary insured and the omitted party to unnecessary risks.

People often misinterpret the location of covered operations. This section must clearly specify where the additional insured's operations will take place. Failing to provide this information can result in coverage gaps, leaving parties unprotected during critical operations.

Inadequate attention to the scope of operations is another common oversight. The endorsement is intended to cover liabilities arising from specific acts or omissions related to the ongoing operations. If the scope is not clearly defined, it may lead to disputes about what is covered under the policy.

Some individuals mistakenly believe that the endorsement automatically extends broader coverage than what is stipulated in their contracts. This misunderstanding can lead to serious implications. It is vital to remember that the coverage provided to additional insureds will not exceed what is required by the underlying contract.

Another error arises when the limits of insurance are not properly understood or communicated. The endorsement specifies that the maximum amount payable is either the contractually required limit or the available limits of insurance, whichever is less. Misunderstanding this can lead to financial exposure in the event of a claim.

Individuals sometimes overlook the importance of reviewing the exclusions section. The endorsement contains specific exclusions that can significantly impact coverage. Not being aware of these exclusions can lead to unpleasant surprises when a claim is filed.

Inaccurate completion of the form can also occur when individuals provide incomplete information. Every field must be filled out completely to ensure that the endorsement is valid. Incomplete forms can be rejected, resulting in a lack of coverage.

Finally, failing to keep a copy of the completed endorsement for personal records is a mistake that can have long-term consequences. Having documentation readily available is essential for reference and can be critical in case of a dispute or claim.

Filling out the CG 20 10 07 04 Liability Endorsement form is a straightforward process. This form allows you to add additional insured parties to your commercial general liability policy. It’s essential to complete this form accurately to ensure that all necessary parties are covered under your policy. Follow the steps below to fill out the form correctly.

Once you have filled out the form, review it for any errors or omissions. Ensure that all information is accurate and complete before submitting it to your insurance provider. This will help prevent any delays in coverage for the additional insured parties.

Consolation Bracket - The path to victory continues for teams in this bracket.

S Corp Form 2553 - You may need to provide additional documentation when filing IRS 2553.

When dealing with the transfer of ownership, utilizing a California Motor Vehicle Bill of Sale form is essential to prevent any misunderstandings in the transaction. This document not only protects both parties but also establishes a clear history of the sale. For those looking for additional resources and templates, you can refer to the Templates and Guide to make the process even easier.

Signing Over Parental Rights in Sc - It is essential for the affiant to fully understand the ramifications of relinquishing rights.