Promissory Note Form for the State of California

Promissory Note Form for the State of California

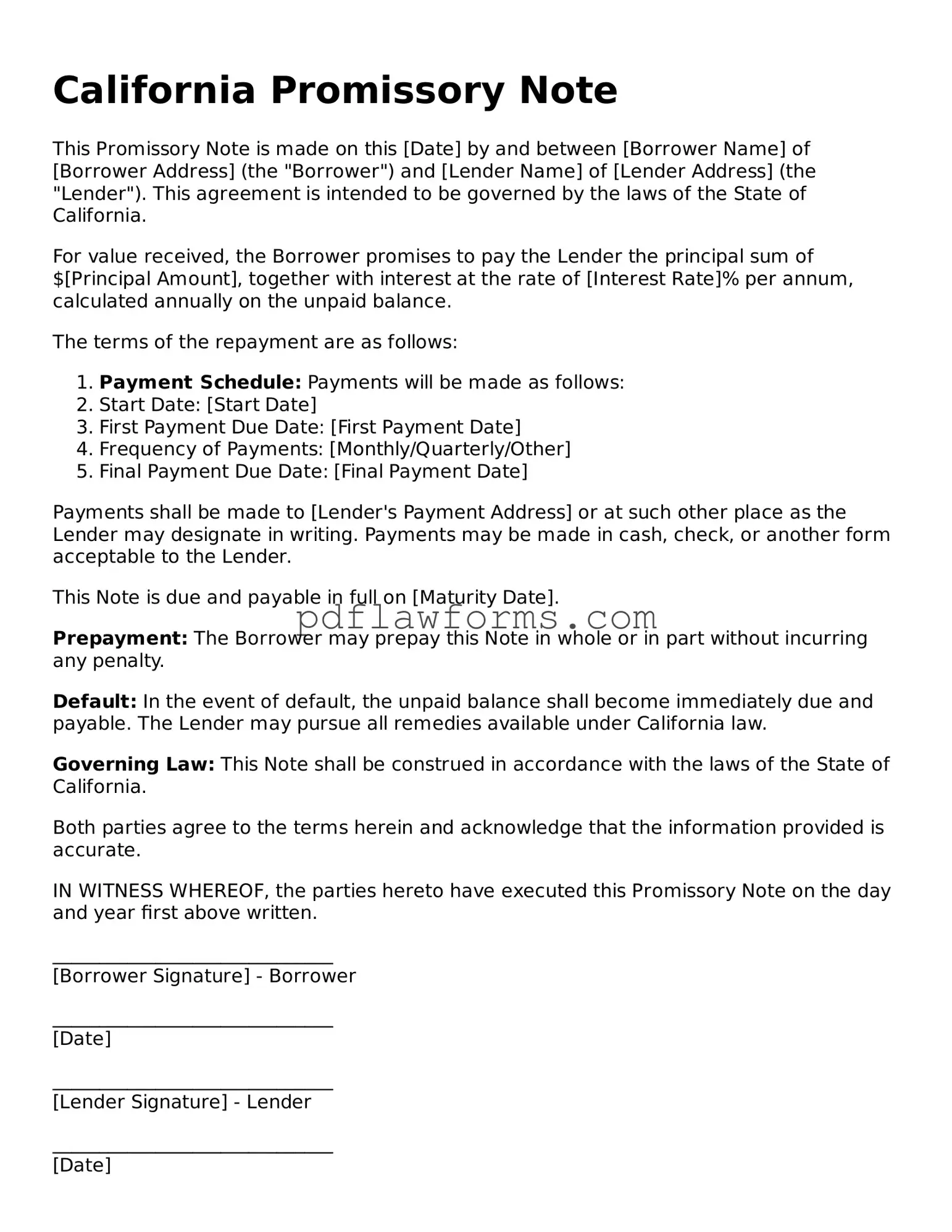

The California Promissory Note form serves as a crucial document in financial transactions, providing a clear outline of the terms under which one party borrows money from another. This form details essential elements such as the principal amount, interest rate, repayment schedule, and any applicable fees. It also specifies the rights and responsibilities of both the borrower and the lender, ensuring that all parties understand their obligations. The document can be customized to fit various situations, whether for personal loans, business financing, or real estate transactions. Clarity and transparency are vital, as they help prevent misunderstandings and disputes down the line. Additionally, the Promissory Note may include provisions for default, allowing lenders to take necessary actions if the borrower fails to meet their obligations. Understanding the importance of this form can lead to smoother financial dealings and a more secure lending environment.

Understanding the California Promissory Note form is crucial for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion. Here are eight common misconceptions:

Clarifying these misconceptions can help ensure that both lenders and borrowers understand their rights and obligations under California law.

When filling out the California Promissory Note form, individuals often make several common mistakes that can lead to complications. One frequent error is failing to include all necessary information. This includes not only the names of the borrower and lender but also the correct addresses and contact details. Omitting any of this information can create confusion and may delay the process.

Another mistake is not specifying the loan amount clearly. The amount should be written both in numerical form and in words to avoid any ambiguity. If the figures do not match, it could lead to disputes later on. Clarity in this section is crucial to ensure that both parties understand the terms of the loan.

People also often overlook the importance of detailing the interest rate. Some may leave it blank or write it ambiguously. It is essential to state whether the interest is fixed or variable and to specify the exact rate. This information is vital for both parties to understand their financial obligations.

Additionally, many individuals fail to include a repayment schedule. This section should outline how and when payments will be made. Without a clear repayment plan, misunderstandings can arise, leading to potential legal issues. A well-defined schedule helps both parties stay on track and maintain clear communication.

Lastly, signatures are sometimes missing or improperly executed. Each party must sign and date the document. If a signature is missing, the note may not be legally binding. Ensuring that all signatures are present and correctly dated is essential for the validity of the agreement.

After obtaining the California Promissory Note form, you are ready to fill it out. This document will require specific information related to the loan agreement. Ensure you have all necessary details at hand before starting the process.

Once completed, review the form for accuracy. Ensure all information is correct and legible before finalizing the document. Keep a copy for your records and provide the original to the lender.

Promissory Note Download - In the event of a dispute, the promissory note serves as the primary reference for resolving issues.

For those looking to document their transaction properly, our guide offers a comprehensive Mobile Home Bill of Sale, ensuring all necessary details are captured during the sale process. To access the form and initiate your paperwork, visit this resource.

Promissory Note Template Florida - Both the lender and the borrower should retain copies of the promissory note for their records.

Free Promissory Note Template Illinois - A written agreement can help avoid misunderstandings in a loan transaction.