Loan Agreement Form for the State of California

Loan Agreement Form for the State of California

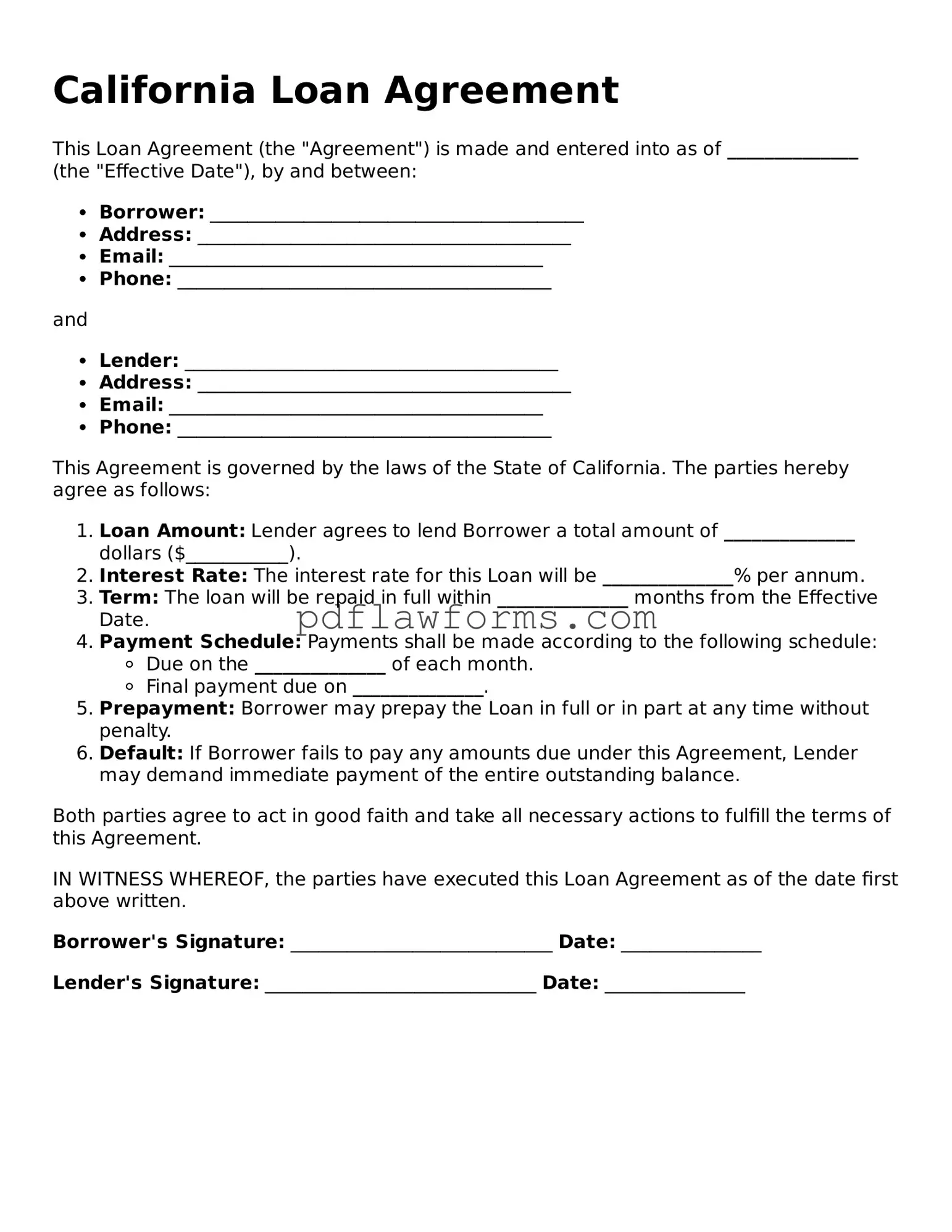

The California Loan Agreement form is an essential document that outlines the terms and conditions of a loan between a lender and a borrower. This form serves as a clear framework for the financial transaction, detailing critical components such as the loan amount, interest rate, repayment schedule, and any applicable fees. It also specifies the rights and obligations of both parties, ensuring that expectations are aligned from the outset. In addition to these core elements, the agreement may include provisions for default, collateral requirements, and dispute resolution procedures. Understanding this form is vital for anyone involved in lending or borrowing money in California, as it helps protect the interests of both parties and provides a legally binding reference should any issues arise during the loan term. By clearly articulating the terms, the California Loan Agreement form fosters transparency and trust, facilitating smoother financial interactions.

Understanding the California Loan Agreement form can be challenging. Here are nine common misconceptions that people often have about this important document.

Each loan agreement is unique and tailored to the specific terms agreed upon by the lender and borrower. Variations can exist based on the type of loan, interest rates, and repayment terms.

While the agreement outlines specific terms, borrowers can often negotiate aspects like interest rates or repayment schedules before signing.

Loan agreements can be used for both large and small amounts. Even personal loans for minor expenses can require a formal agreement.

It is crucial to read and understand the entire agreement before signing. Ignoring the details can lead to misunderstandings and potential financial issues.

Lenders may have different policies and terms. It’s important to shop around and compare offers from various lenders.

While the agreement is binding, amendments can be made if both parties agree to the changes in writing.

Businesses also use loan agreements. Companies often enter into loan agreements to secure funding for operations or expansion.

Defaulting can lead to serious repercussions, including damage to credit scores, legal action, and loss of collateral.

While laws may vary, many aspects of California loan agreements can be enforceable in other states, especially if the lender operates across state lines.

By dispelling these misconceptions, borrowers can approach the California Loan Agreement form with greater confidence and understanding.

When filling out the California Loan Agreement form, many individuals make common mistakes that can lead to complications later on. One frequent error is not providing accurate personal information. It is essential to double-check names, addresses, and contact details to ensure they are correct. Any discrepancies can cause delays or issues in processing the loan.

Another mistake is failing to read the terms and conditions carefully. Many people overlook important clauses that outline their responsibilities and rights. Understanding these terms is crucial to avoid misunderstandings and potential disputes down the line.

Some individuals neglect to include all necessary documentation when submitting the form. Required documents often include proof of income, identification, and credit history. Missing any of these can result in a rejection of the application or further delays.

Additionally, not specifying the loan amount clearly can lead to confusion. It is vital to state the exact amount being requested. Ambiguities can cause lenders to misinterpret the application, which may lead to unfavorable outcomes.

People sometimes make the mistake of not understanding the repayment terms. It is important to clarify the interest rate, payment schedule, and any fees associated with the loan. Misunderstanding these terms can create financial strain in the future.

Another common error is not signing the agreement where required. An unsigned document is not legally binding. Ensure that all parties involved have signed and dated the form before submission.

Some applicants also rush through the process, which can lead to careless mistakes. Taking the time to review the form thoroughly can prevent errors that may complicate the loan approval process.

Lastly, overlooking communication with the lender can be detrimental. Keeping an open line of communication ensures that any questions or concerns are addressed promptly. This proactive approach can help facilitate a smoother transaction.

Filling out the California Loan Agreement form is a straightforward process. This document will require some specific information from both the lender and the borrower. Once completed, it serves as a binding agreement that outlines the terms of the loan, ensuring clarity and protection for both parties involved.

After completing these steps, both parties should review the agreement to ensure all details are accurate. Having a clear understanding of the terms can help prevent misunderstandings in the future.

Promissory Note Florida Pdf - Signatures from both parties make the agreement valid and enforceable.

When renting property in Illinois, understanding the specifics of a vital Lease Agreement template can help ensure compliance with local laws and protect both parties involved. This form will guide you through important elements such as rental terms, maintenance responsibilities, and payment schedules, allowing for a smoother leasing experience.