Official Business Purchase and Sale Agreement Form

Official Business Purchase and Sale Agreement Form

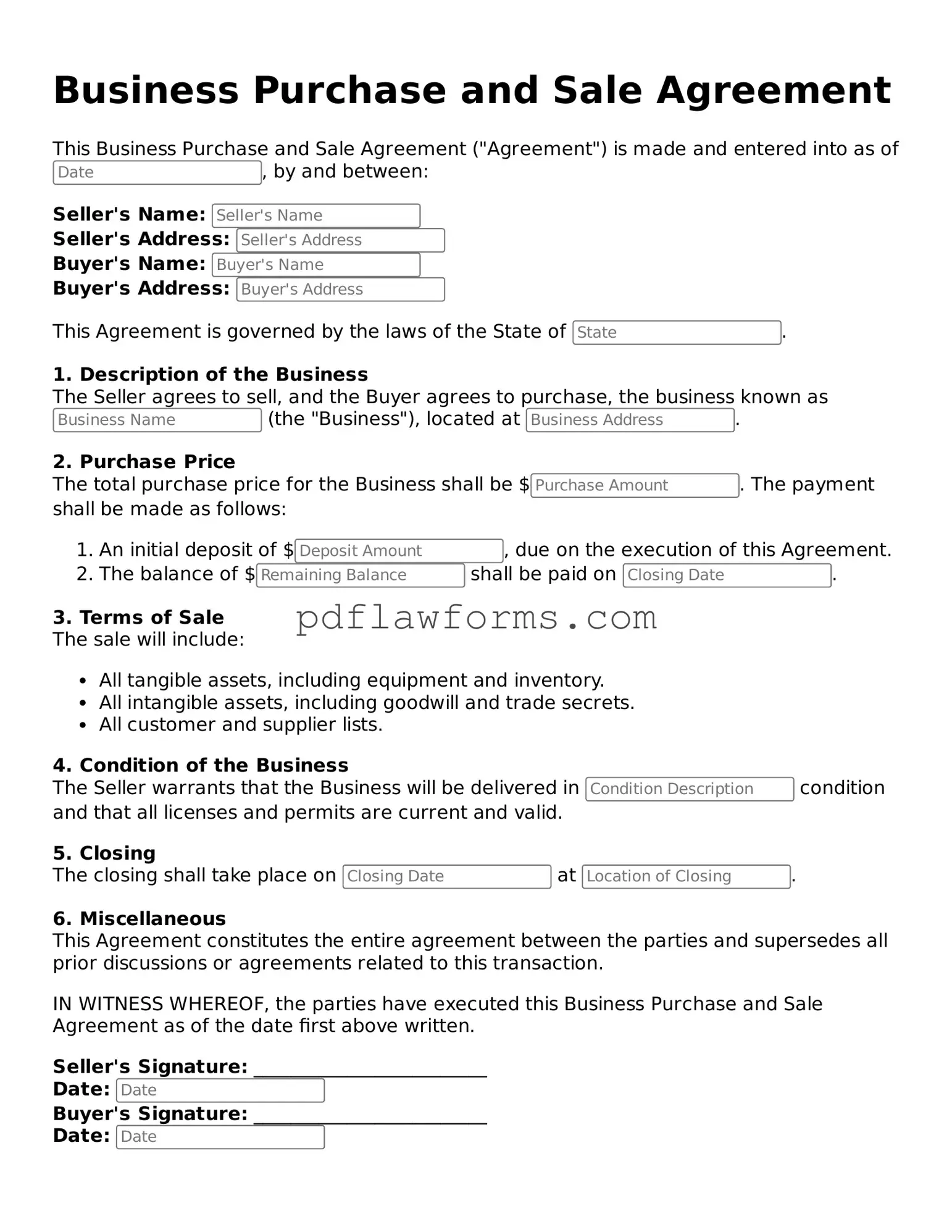

When engaging in the transfer of business ownership, a Business Purchase and Sale Agreement (BPSA) serves as a crucial document that outlines the terms and conditions of the transaction. This agreement typically includes essential elements such as the purchase price, payment terms, and the assets being sold, which can range from physical inventory to intellectual property. Additionally, the BPSA addresses representations and warranties made by both the buyer and the seller, ensuring that both parties have a clear understanding of their obligations and rights. Contingencies may also be specified, allowing for conditions that must be met before the sale can proceed. Furthermore, the agreement often includes provisions for confidentiality and non-compete clauses, protecting the interests of both parties post-sale. By clearly delineating these aspects, the Business Purchase and Sale Agreement helps to mitigate risks and provides a framework for a smooth transition of ownership.

Understanding the Business Purchase and Sale Agreement (BPSA) is crucial for anyone involved in buying or selling a business. However, several misconceptions can lead to confusion. Here are nine common misconceptions about the BPSA:

Clarifying these misconceptions can help buyers and sellers navigate the complexities of business transactions more effectively.

When completing a Business Purchase and Sale Agreement, it’s crucial to be thorough and accurate. One common mistake people make is neglecting to provide complete information about the parties involved. This includes not only the names of the buyer and seller but also their addresses and contact details. Incomplete information can lead to confusion and potential disputes later on.

Another frequent error is failing to specify the terms of the sale. This includes not detailing the purchase price, payment terms, and any contingencies. Vague terms can create misunderstandings and may leave one party feeling dissatisfied with the agreement. It is essential to be clear and precise about what is being sold and under what conditions.

People often overlook the importance of including representations and warranties in the agreement. These statements provide assurances about the condition of the business being sold. Without these, buyers may find themselves facing unexpected issues after the sale is finalized. It’s wise to outline what the seller guarantees about the business, such as its financial status or legal compliance.

Another mistake is ignoring the need for a timeline. A well-structured agreement should include important dates, such as the closing date and any deadlines for due diligence. Without a clear timeline, both parties may have different expectations, which can lead to frustration and delays.

Lastly, many individuals forget to consult with professionals such as attorneys or accountants before finalizing the agreement. While it may seem like an extra step, expert advice can help identify potential pitfalls and ensure that the agreement complies with all relevant laws. Skipping this step can result in costly mistakes that could have been easily avoided.

After gathering the necessary information and documents, you are ready to fill out the Business Purchase and Sale Agreement form. This document will guide you through the sale or purchase of a business, ensuring that all parties are clear on the terms and conditions of the transaction.

After completing the form, review it for accuracy. Both parties should retain a copy for their records. This agreement serves as a crucial step in formalizing the sale and protecting the interests of everyone involved.

Codicil Template - A codicil can outline special conditions tied to inheritances.

The General Bill of Sale form is not only a crucial document for transferring ownership of a tangible item, but it can also be easily obtained through resources like My PDF Forms. This essential legal tool protects both the seller and the buyer by providing a clear record of the transaction. Understanding its components and usage is crucial for anyone involved in buying or selling personal property.

Shared Well Agreement Template - Parties agree to the right to draw water from a well for domestic use as defined in the contract.