Fill Your Business Credit Application Template

Fill Your Business Credit Application Template

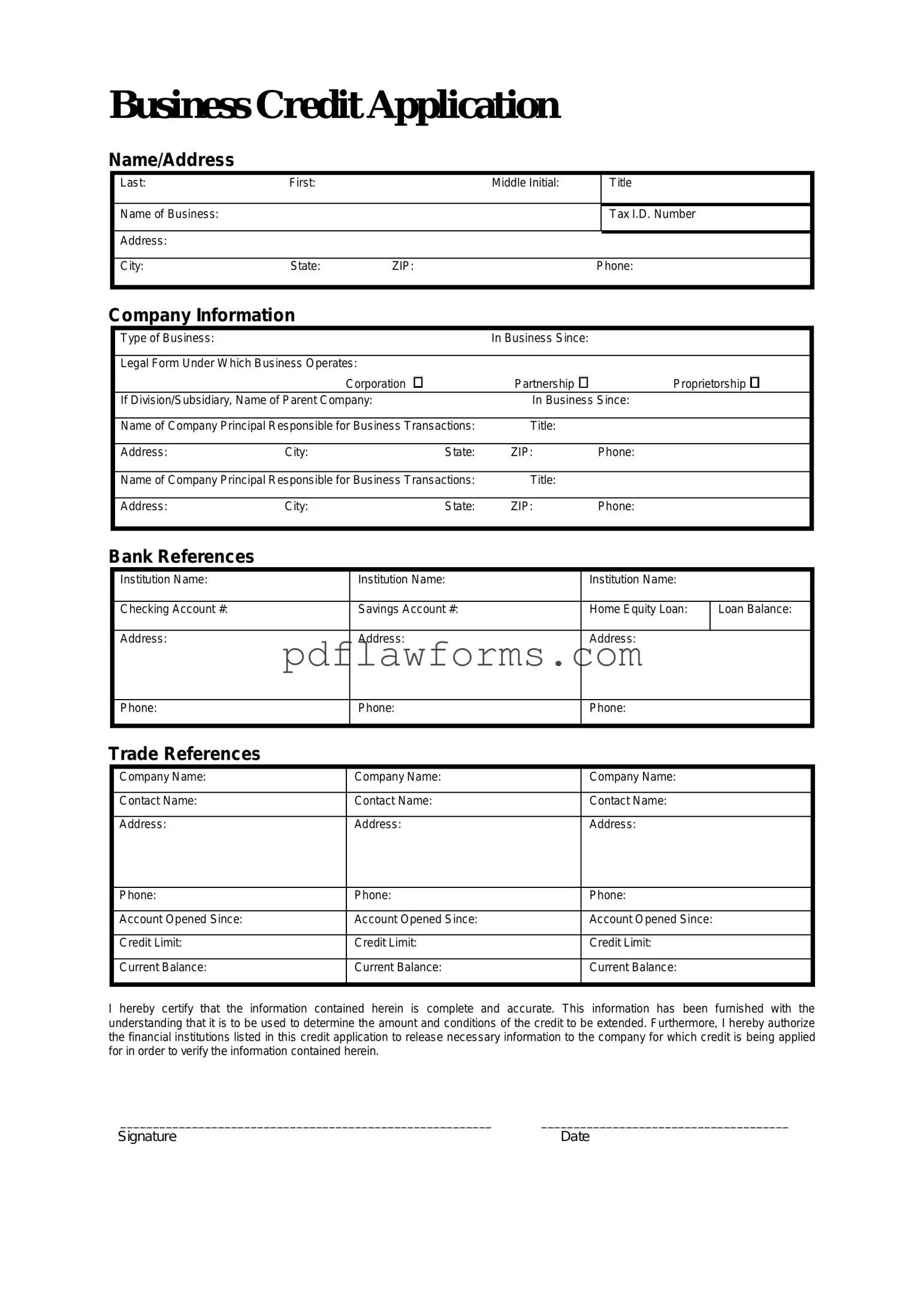

When a business seeks to establish a line of credit with a supplier or lender, the Business Credit Application form plays a crucial role in the process. This form typically requires essential information about the business, including its legal name, address, and type of entity, such as a corporation or LLC. Additionally, it often asks for details about the owners or principal officers, providing insight into the individuals behind the business. Financial information is also a key component, with applicants needing to disclose their annual revenue, credit history, and any outstanding debts. Furthermore, the form may include references from other creditors, allowing the lender to assess the applicant's creditworthiness. By carefully filling out this application, businesses not only present their financial standing but also demonstrate their commitment to transparency and accountability in their financial dealings.

Understanding the Business Credit Application form is crucial for businesses seeking credit. However, several misconceptions can lead to confusion. Here are seven common misunderstandings:

Addressing these misconceptions can help businesses navigate the credit application process more effectively.

Filling out a Business Credit Application form can be a straightforward process, but many people stumble along the way. One common mistake is providing inaccurate or incomplete information. When applicants rush through the form, they may overlook crucial details, such as the business's legal name or address. This can lead to delays in processing the application and may even result in a denial of credit.

Another frequent error involves failing to disclose all necessary financial information. Lenders need a clear picture of the business's financial health. Omitting debts, assets, or income can raise red flags. It’s essential to be transparent and thorough, as incomplete financial disclosures can jeopardize the chances of securing credit.

Many applicants also neglect to check their credit history before submitting the application. A poor credit score can significantly affect the outcome. By reviewing their credit reports in advance, business owners can identify issues and address them before applying. This proactive approach can make a substantial difference in the approval process.

In addition, some individuals forget to include supporting documents. A Business Credit Application often requires additional paperwork, such as tax returns or financial statements. Not providing these documents can slow down the review process. It’s wise to gather all necessary documents beforehand to ensure a smooth application experience.

Lastly, failing to follow up after submitting the application is a mistake that many make. After submitting, it’s important to check in with the lender. This shows initiative and can help clarify any questions they might have. A simple follow-up can keep the application moving forward and demonstrate commitment to the lender.

Once you have the Business Credit Application form ready, you will need to complete it accurately to ensure a smooth review process. Following these steps will help you provide the necessary information clearly.

After completing the form, review it for accuracy. Ensure that all required fields are filled out and that the information is up to date. Submit the application as instructed, and be prepared for any follow-up communication from the creditor.

Notarized Letter of Consent - The consent may also outline emergency contact procedures for minors on board.

When engaging in the motorcycle purchasing process, it is important to have a comprehensive understanding of the necessary documentation required for a smooth transaction. One such document is the California Motorcycle Bill of Sale, which facilitates the legal transfer of ownership and proves the sale has taken place. For those looking to simplify this process, resources like Templates and Guide can provide valuable assistance in ensuring all information is correctly captured and conforms to state requirements.

What Is Osha 300 - Tracks both minor and severe incidents to improve overall safety practices.