Official Business Bill of Sale Form

Official Business Bill of Sale Form

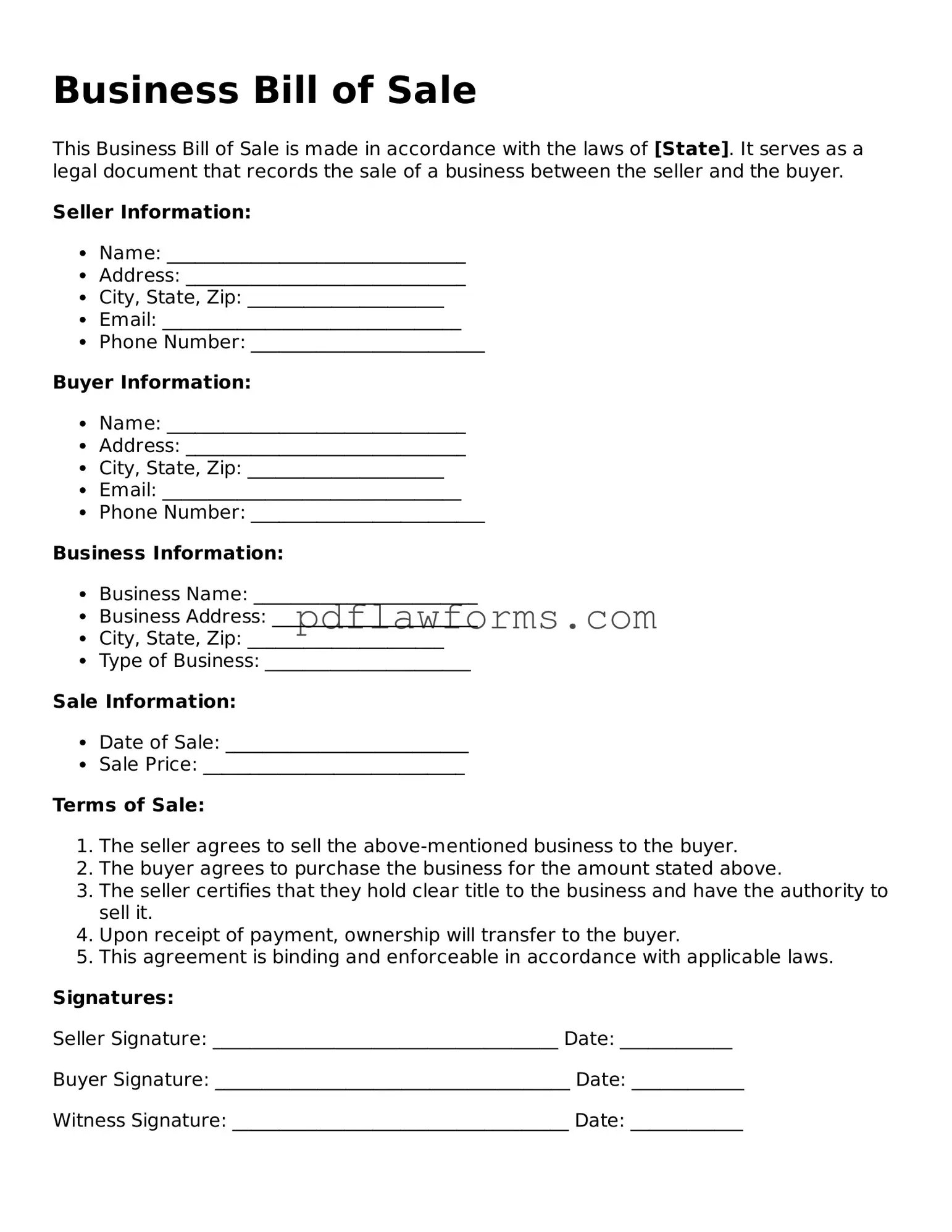

The Business Bill of Sale form serves as a crucial document in the transfer of ownership of a business or its assets. This form outlines the specific terms of the sale, including the names of the buyer and seller, a detailed description of the business or assets being sold, and the agreed-upon purchase price. It also typically includes information regarding any warranties or representations made by the seller, which can protect the buyer from future liabilities. Essential elements such as the date of the transaction and the signatures of both parties are necessary to validate the agreement. Furthermore, the form may address any conditions or contingencies related to the sale, ensuring that both parties have a clear understanding of their rights and responsibilities. By providing a written record of the transaction, the Business Bill of Sale form not only facilitates a smoother transfer of ownership but also serves as a legal safeguard in the event of disputes or misunderstandings in the future.

Understanding the Business Bill of Sale form is essential for anyone engaged in the sale or purchase of a business. However, several misconceptions can lead to confusion. Below is a list of seven common misunderstandings regarding this important document.

By addressing these misconceptions, individuals can better navigate the complexities of business transactions and ensure that their interests are adequately protected.

Filling out a Business Bill of Sale form is a crucial step in transferring ownership of a business. However, many people make common mistakes that can lead to complications down the line. Understanding these pitfalls can help ensure a smooth transaction.

One frequent error is not providing complete information. It's essential to include all relevant details, such as the names and addresses of both the buyer and seller. Omitting this information can create confusion and may lead to disputes later on.

Another mistake is failing to accurately describe the business being sold. This includes not just the name of the business but also its assets, liabilities, and any relevant licenses or permits. A vague description can lead to misunderstandings about what is included in the sale.

People often overlook the importance of including a sales price. Without a clearly stated amount, it becomes challenging to establish the value of the transaction. This can affect everything from tax obligations to future negotiations.

Some individuals neglect to indicate the payment method. Whether the buyer is paying in cash, through financing, or with a trade, specifying the payment method is crucial. This clarity helps both parties understand their obligations and can prevent disputes.

Another common mistake is not having the document signed by both parties. A Business Bill of Sale is only valid if both the buyer and seller sign it. Failing to do so can render the document ineffective, leaving the transaction open to challenges.

People sometimes forget to date the document. Including the date of the transaction is important for legal purposes. It establishes when the ownership transfer took place and can be critical for record-keeping.

In some cases, individuals fail to consult a professional before completing the form. Legal and financial advisors can provide valuable insights and help ensure that the document meets all necessary requirements. Skipping this step can lead to costly mistakes.

Another mistake is not keeping a copy of the completed form. Once the transaction is finalized, it’s vital to retain a copy for your records. This can be useful for future reference, especially if questions arise about the sale.

Finally, people may ignore local laws and regulations. Each state has its own requirements for a Business Bill of Sale. Familiarizing yourself with these rules can prevent legal issues that may arise from non-compliance.

By being aware of these common mistakes, individuals can navigate the process of completing a Business Bill of Sale more effectively. Attention to detail and a proactive approach can lead to a successful business transaction.

After gathering the necessary information, you are ready to fill out the Business Bill of Sale form. This document will help you officially transfer ownership of a business. Follow these steps to ensure you complete the form accurately.

Once you have filled out the form, review it for any errors or omissions. This step is crucial to avoid complications in the future.

Golf Cart Bill of Sale Texas - Helps establish a fair market value for the cart.

In addition to the legal protection offered by the form, sellers and buyers may find it beneficial to access resources and templates to streamline the process, such as those available at Templates and Guide, ensuring a smooth transaction that meets all requirements.

How to Write a Bill of Sale for a Boat - The document can be an invaluable asset when it comes to engaging in future sales or trades of the boat.